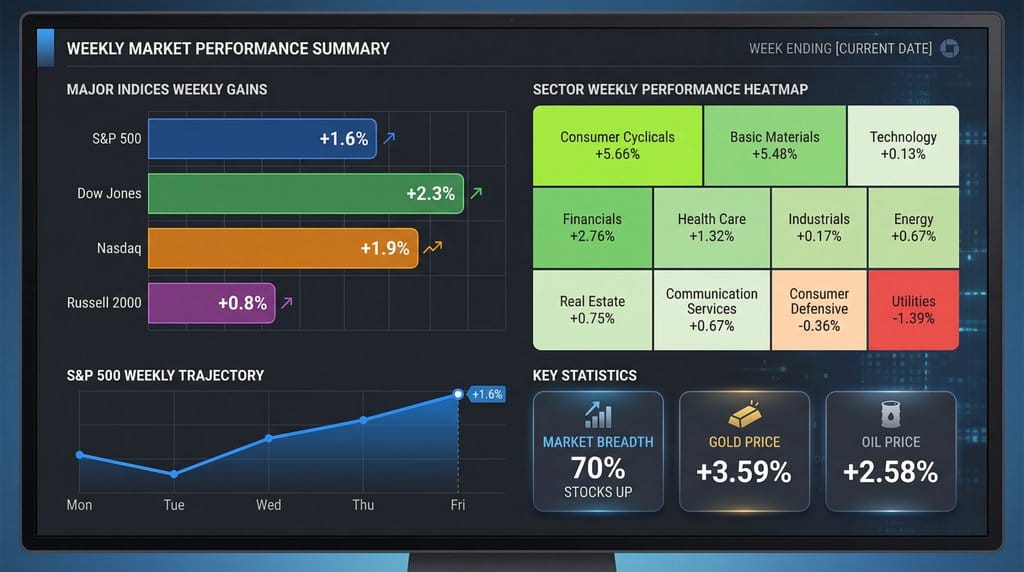

Week in Review: Market Performance

The first full trading week of 2026 saw US equity markets surge to new heights, with the S&P 500 and Dow Jones Industrial Average closing at record highs. Investor optimism was fueled by a combination of factors, including a resilient labor market, strong corporate earnings, and continued enthusiasm for the technology sector. The S&P 500 gained approximately 1.6% for the week, closing at 6,966.28. The Dow Jones Industrial Average posted a weekly gain of 2.3%, ending at 49,504.07, marking its best five-day start to a year. The tech-heavy Nasdaq Composite also had a strong showing, rising by about 1.9%, while the small-cap Russell 2000 added 0.8%. Market breadth was positive, with approximately 70% of US-listed stocks advancing for the week, indicating broad participation in the rally. The overall market theme was one of risk-on sentiment, as investors shrugged off lingering concerns about inflation and geopolitical tensions.

Major Market Drivers

Several key developments drove market performance this week. The December jobs report, released on Friday, showed the US economy added 50,000 jobs, below economists' expectations. However, the unemployment rate unexpectedly ticked down to 4.4%, reinforcing the narrative of a resilient labor market. This solidified expectations that the Federal Reserve will hold interest rates steady at its upcoming meeting. Investment implications: A steady Fed and a strong labor market create a positive backdrop for equities, although wage growth and inflation data will be closely watched for any signs of overheating.

Another significant driver was the continued focus on President Trump's economic policies. The Supreme Court is expected to rule on the legality of his sweeping tariffs next week, creating some uncertainty. However, the market seemed to focus more on the pro-growth aspects of his agenda, including a new initiative to have Freddie Mac and Fannie Mae purchase $200 billion in mortgage-backed securities to boost the housing market. Investment implications: The outcome of the tariff ruling could introduce significant volatility, while the mortgage-backed security purchase program could benefit the housing and financial sectors.

In geopolitical news, developments in Venezuela captured the attention of the energy markets. The Trump administration is taking a more active role in the country's oil industry, with plans for US companies to invest heavily in rebuilding its infrastructure. Investment implications: This could lead to increased oil production from Venezuela, potentially impacting global oil prices and benefiting the involved US energy companies.

Finally, the semiconductor sector had a stellar week, driven by positive announcements at the CES technology conference and supportive comments from President Trump about bringing chip manufacturing back to the US. Intel, in particular, saw its stock surge after the President praised its CEO. Investment implications: The reshoring of semiconductor manufacturing is a powerful long-term theme that could continue to drive investment in the sector.

Sector Performance Analysis

The week saw a clear rotation into cyclical sectors, with Consumer Cyclicals (+5.66%) and Basic Materials (+5.48%) leading the pack. This suggests that investors are becoming more confident in the economic outlook and are willing to take on more risk. The technology sector, while still a strong performer, lagged behind the cyclical leaders with a gain of just 0.13%. The laggard for the week was the defensive Utilities sector, which fell by 1.39%. Investment implications: The outperformance of cyclical sectors and the underperformance of defensive sectors is a classic risk-on signal. This trend could continue if economic data remains positive.

What We Learned This Week

This week reinforced the market's ability to look past short-term uncertainties and focus on the longer-term growth narrative. Despite a mixed jobs report and the looming Supreme Court tariff decision, investors chose to focus on the positives, such as the resilient labor market and the potential for pro-growth policies. The market's sentiment has clearly shifted to a more risk-on posture, as evidenced by the rotation into cyclical sectors. Investment implications: Investors should be mindful of the prevailing optimism but also be prepared for potential volatility, especially around the upcoming tariff ruling. The week's action suggests that a buy-the-dip mentality remains firmly in place.

Looking Ahead: Next Week's Focus

Next week is shaping up to be another eventful one, with a packed economic calendar and several key events to watch. The main focus will be on the release of the Consumer Price Index (CPI) and Producer Price Index (PPI) reports, which will provide crucial insights into the inflation picture. The Supreme Court's potential ruling on tariffs on Wednesday could also be a major market-moving event. In terms of Fed speakers, several officials are scheduled to speak, including Vice Chair Philip N. Jefferson and Vice Chair for Supervision Michelle W. Bowman. Finally, earnings season will kick off with reports from major banks, including JPMorgan Chase, Bank of America, and Wells Fargo. Investment implications: Investors should be prepared for potential volatility around the inflation data and the tariff ruling. The bank earnings will provide a key reading on the health of the financial sector and the broader economy.

Disclaimer: This analysis is for informational and educational purposes only and should not be considered financial advice. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.