Economic Week in Review

The first full trading week of 2026 was characterized by a complex interplay of slowing economic growth and persistent inflationary signals. The U.S. labor market, a key focus for investors and policymakers, showed signs of cooling, with job creation moderating and the unemployment rate remaining elevated. However, wage growth accelerated, suggesting that inflationary pressures are not yet fully contained. This dynamic has created a challenging environment for the Federal Reserve, which is attempting to balance its dual mandate of price stability and maximum employment. Meanwhile, international data presented a mixed picture, with European inflation stabilizing and China's economy showing resilience. The week's market performance reflected this uncertainty, with U.S. equities posting modest losses while international stocks outperformed, aided by a weaker dollar. The week ahead will be crucial in providing further clarity on the economic trajectory, with the release of the December jobs report and other key indicators.

Investment implications: The current environment of slowing growth and persistent inflation, often referred to as “stagflation-lite,” presents a challenging landscape for investors. A defensive portfolio posture may be warranted, with a focus on quality companies with strong balance sheets and pricing power. Sectors that tend to perform well in inflationary environments, such as energy and materials, may also be worth considering. Investors should also be mindful of the potential for increased market volatility as the Federal Reserve navigates the delicate balance between controlling inflation and supporting economic growth.

Deep Dive: Key Data Points

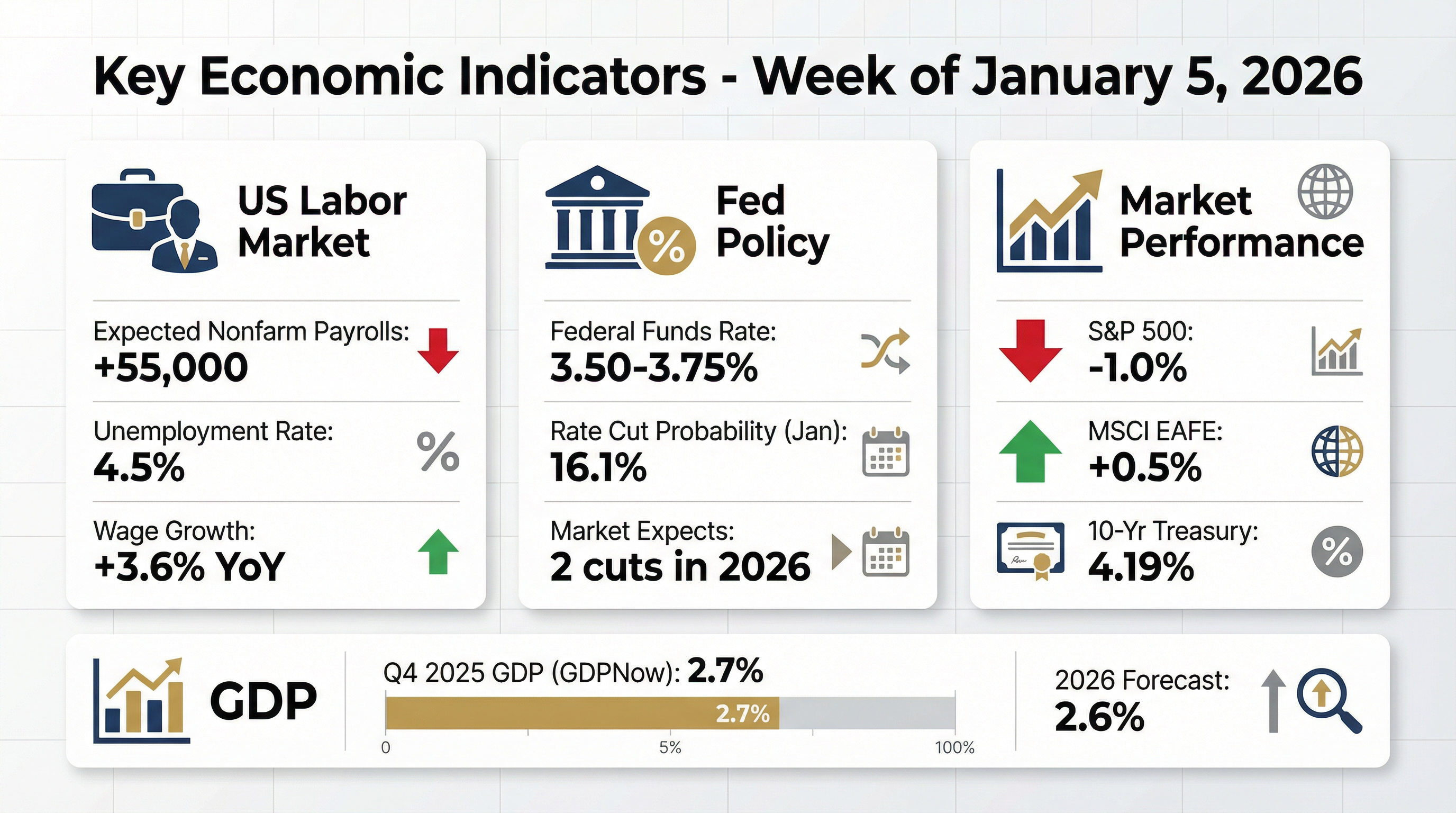

The most significant data point of the week was the slew of labor market indicators pointing to a continued slowdown. The December jobs report is expected to show a further moderation in nonfarm payrolls, with consensus estimates around 55,000, down from 64,000 in November. The unemployment rate is anticipated to edge lower to 4.5% from a more than four-year high of 4.6%. While a lower unemployment rate is typically a positive sign, the overall trend of slowing job growth suggests a weakening labor market. The JOLTS job openings data for November also pointed to a decrease in labor demand. This cooling of the labor market is a welcome development for the Federal Reserve in its fight against inflation, as it should help to ease wage pressures over time.

However, the latest average hourly earnings data presented a conflicting signal. The forecast for December is a 0.3% month-over-month increase, up from 0.1% in November, and a 3.6% year-over-year increase. This acceleration in wage growth suggests that inflationary pressures remain entrenched in the economy. This “sticky” wage inflation is a key concern for the Fed, as it can lead to a wage-price spiral, where higher wages lead to higher prices, which in turn lead to demands for even higher wages. The ISM PMI surveys for December are also expected to signal a continued contraction in the manufacturing sector and a modest slowdown in services activity, further adding to the picture of a slowing economy.

Investment implications: The conflicting signals from the labor market create a difficult environment for investors to navigate. On the one hand, a slowing labor market could give the Fed more room to ease monetary policy, which would be positive for risk assets. On the other hand, persistent wage inflation could force the Fed to keep interest rates higher for longer, which would be a headwind for stocks and bonds. In this environment, investors should focus on companies with strong pricing power that can pass on rising labor costs to consumers. A focus on quality and value stocks may also be prudent. For fixed-income investors, the current environment may favor shorter-duration bonds, which are less sensitive to changes in interest rates.

Fed Policy & Interest Rate Outlook

The Federal Reserve is facing a delicate balancing act. After cutting interest rates three times in 2025, the market is now pricing in two more cuts in 2026. However, the Fed's own projections from December suggest only one rate cut this year. This divergence in expectations is a source of market uncertainty. The CME FedWatch Tool currently indicates a 16.1% probability of a 25 basis point rate cut at the January 29 meeting, and a 16.6% probability of a cut at the March 19 meeting. These low probabilities suggest that the market is not convinced that the Fed will act in the near term.

The debate within the Fed is also a key factor to watch. Some officials, like Governor Stephen Miran, are arguing for more aggressive rate cuts, citing the restrictive stance of monetary policy. Others, like Richmond Fed President Thomas Barkin, are more cautious, emphasizing the need for “finely tuned” judgments. The Fed's preferred measure of inflation, the Personal Consumption Expenditures (PCE) price index, was at 2.8% as of September 2025, still above the Fed's 2% target. This will likely keep the more hawkish members of the committee on alert.

Investment implications: The uncertainty surrounding Fed policy is a major risk for investors. If the Fed is more hawkish than the market expects, it could lead to a sell-off in both stocks and bonds. Conversely, a more dovish Fed could provide a tailwind for risk assets. In this environment, investors should consider strategies that can perform well in a variety of interest rate scenarios. This could include a barbell strategy in fixed income, with a mix of short-term and long-term bonds. For equity investors, a focus on companies with low debt levels and strong cash flows may be beneficial, as they are less vulnerable to rising interest rates.

Cross-Asset Impact Analysis

The cross-asset performance in the first week of 2026 reflected the prevailing economic uncertainty. U.S. stocks, as measured by the S&P 500, declined by 1.0%, with the tech-heavy NASDAQ falling 1.5%. This underperformance of growth-oriented stocks is typical in an environment of rising interest rates and economic uncertainty. In contrast, international equities, as measured by the MSCI EAFE index, gained 0.5%, benefiting from a weaker U.S. dollar. The dollar has been a significant headwind for international returns in recent years, but its depreciation in 2025 has provided a tailwind.

In the bond market, the 10-year Treasury yield remained relatively stable at 4.19%. This suggests that the bond market is pricing in a slowdown in economic growth, but is also wary of persistent inflation. Gold experienced significant volatility, with a sharp decline in late December followed by a rebound in the new year. This price action reflects the conflicting forces of a stronger dollar (which is typically negative for gold) and safe-haven demand amid geopolitical tensions and economic uncertainty. Oil prices rose 1.0% for the week, supported by ongoing supply constraints and a weaker dollar.

Investment implications: The current cross-asset dynamics suggest that a diversified portfolio is more important than ever. The underperformance of U.S. stocks and the outperformance of international equities highlight the potential benefits of global diversification. The stability of Treasury yields suggests that bonds can still play a valuable role in a portfolio as a hedge against equity market volatility. Gold remains a volatile but potentially useful hedge against inflation and geopolitical risk. The case for diversification is strengthening as earnings growth is expected to broaden beyond the mega-cap tech stocks that have dominated the market in recent years. The closing of the growth gap between the U.S. and international economies, combined with a weaker dollar, also supports a more global approach to equity investing.

Week Ahead: Economic Calendar

The week ahead will be packed with important economic data releases that will provide further clarity on the economic outlook. The main event will be the December jobs report on Friday, which will be closely watched for signs of further cooling in the labor market. The ADP employment report and JOLTS job openings data will also provide additional insights into the labor market. The ISM PMI surveys for December will give a reading on the health of the manufacturing and services sectors. The preliminary January reading of the University of Michigan Consumer Sentiment index will provide a timely update on consumer morale.

Outside of the U.S., the focus will be on inflation data from Europe and China. The Eurozone, Germany, France, and Italy will all release their preliminary inflation readings for December. In China, the RatingDog Services PMI and inflation data will be closely watched for signs of the effectiveness of the government's policy support. India will release its FY26 GDP growth estimates, and Australia will report its November inflation data.

Investment implications: The upcoming data releases have the potential to move markets. A weaker-than-expected jobs report could increase the probability of a Fed rate cut, which would likely be positive for risk assets. However, a hot inflation report from Europe could put pressure on the European Central Bank to maintain its hawkish stance, which could be a headwind for global markets. Investors should be prepared for increased volatility around these key data releases. It may be prudent to avoid making large portfolio changes ahead of the data and to maintain a diversified and balanced portfolio.

Disclaimer: This post is for informational purposes only and should not be considered investment advice. The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Market Wealth Pro. Investing in financial markets involves risk, and you should consult with a qualified financial professional before making any investment decisions.