Economic Overview: A Complex Landscape of Growth and Inflation

The United States economy in early 2026 presents a highly complex and somewhat contradictory landscape for investors and policymakers alike. Recent data releases from the Bureau of Economic Analysis, the Bureau of Labor Statistics, and the Federal Reserve paint a picture of an economy that is simultaneously cooling in certain sectors while maintaining stubborn inflationary pressures in others. This divergence is creating significant challenges for monetary policy and asset allocation strategies.

The most striking feature of the current economic environment is the apparent disconnect between slowing economic growth and persistent inflation. While gross domestic product (GDP) growth has decelerated sharply, key inflation metrics remain uncomfortably above the Federal Reserve's long-term target of 2.0 percent. Furthermore, the labor market, which had been a pillar of strength throughout the post-pandemic recovery, is beginning to show undeniable signs of weakness, with unexpected job losses reported in the most recent data.

For investors, this environment necessitates a highly nuanced approach. The traditional playbook of relying on broad market indices may prove less effective in a scenario where economic crosscurrents create distinct winners and losers. Understanding the interplay between these key economic indicators—inflation, employment, and growth—is essential for navigating the volatility and identifying opportunities in the current market cycle.

Inflation & Fed Policy: The Stubborn Last Mile

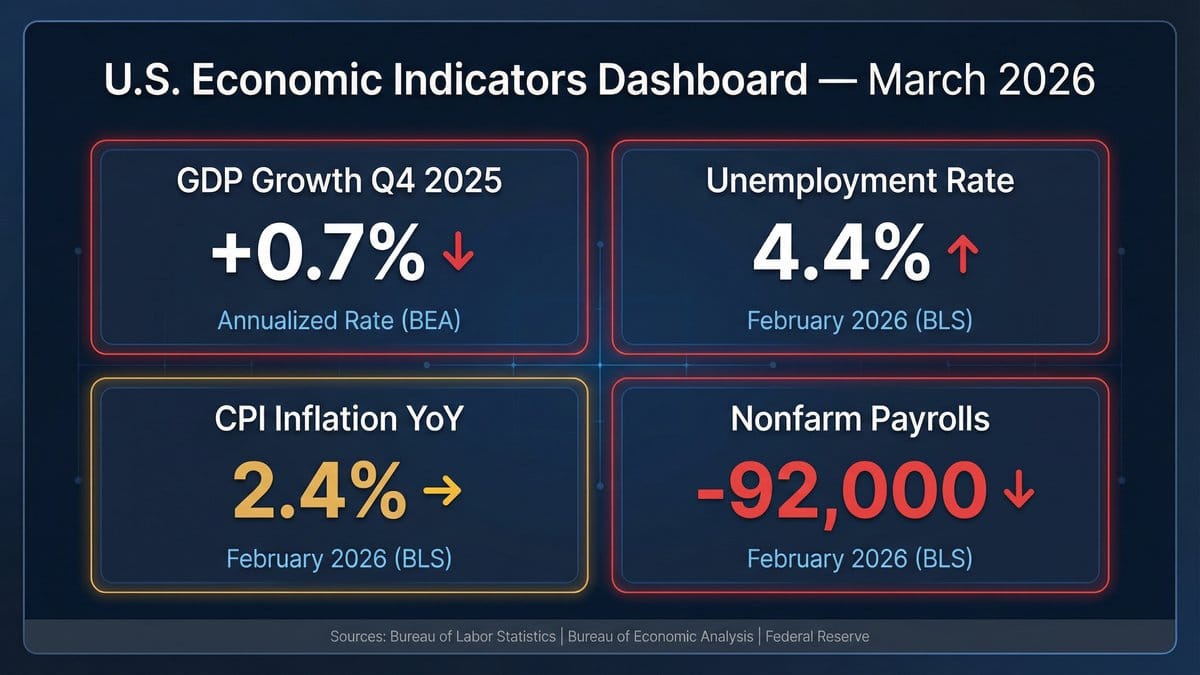

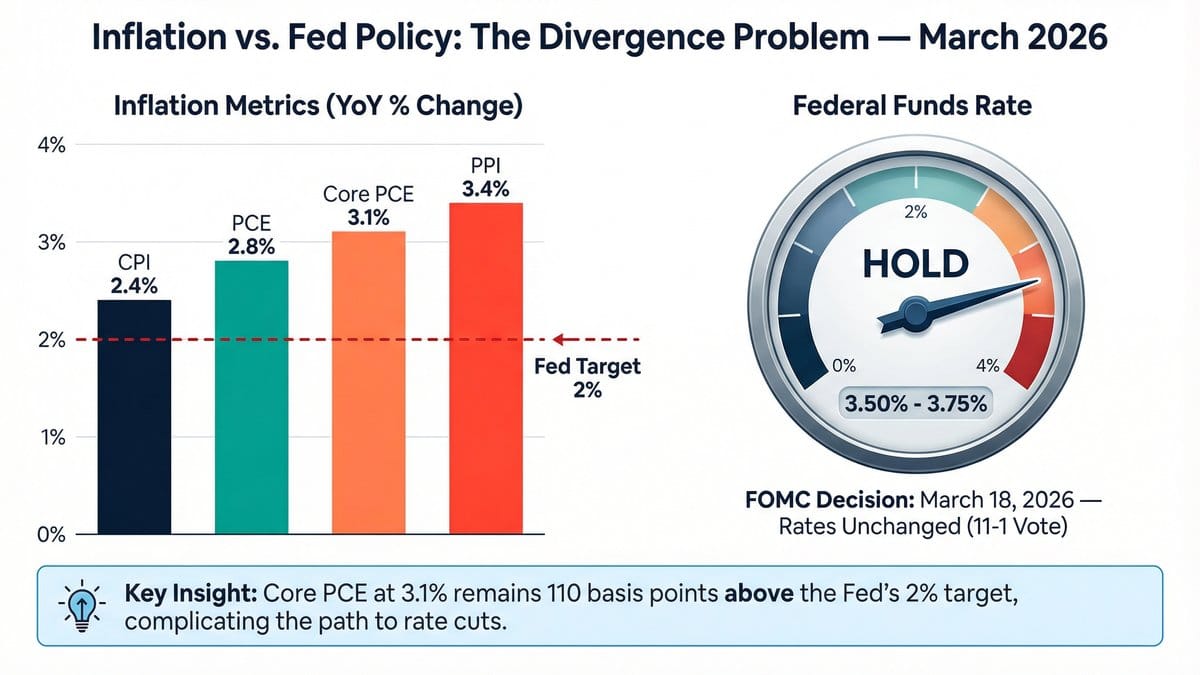

The battle against inflation continues to be the central focus of the Federal Reserve, and recent data indicates that the “last mile” of this fight is proving to be the most difficult. According to the Bureau of Labor Statistics, the Consumer Price Index (CPI) for All Urban Consumers increased by 2.4 percent for the 12 months ending in February 2026. While this represents a significant improvement from the peak inflation rates seen in previous years, it remains stubbornly above the Fed's 2.0 percent target. On a monthly basis, the CPI rose 0.3 percent in February, driven largely by increases in shelter and energy costs.

More concerning for policymakers is the data from the Personal Consumption Expenditures (PCE) price index, which is the Federal Reserve's preferred measure of inflation. The latest data shows PCE inflation at 2.8 percent year-over-year. Even more troubling is the Core PCE, which excludes volatile food and energy prices; it stands at 3.1 percent year-over-year, indicating that underlying inflationary pressures remain entrenched in the economy. Additionally, the Producer Price Index (PPI) for final demand rose 3.4 percent over the 12 months ending in February, suggesting that pipeline price pressures could eventually pass through to consumers.

In response to this persistent inflation, the Federal Open Market Committee (FOMC) voted 11-1 at its March 18, 2026 meeting to maintain the target range for the federal funds rate at 3.50 to 3.75 percent. The Fed's statement emphasized that while economic activity has been expanding at a solid pace, inflation remains “somewhat elevated,” and the Committee remains highly attentive to inflation risks. This “higher for longer” stance on interest rates reflects the central bank's commitment to returning inflation to its 2 percent objective, even at the risk of slowing economic growth.

Investment implications: The persistence of inflation and the Federal Reserve's commitment to maintaining restrictive monetary policy suggest that interest rates will remain elevated for the foreseeable future. This environment is generally unfavorable for long-duration fixed-income assets and highly leveraged growth stocks. Investors should consider allocating capital toward sectors that historically perform well in inflationary environments, such as energy, materials, and companies with strong pricing power. Additionally, short-term Treasury bills and money market funds continue to offer attractive, relatively risk-free yields.

Labor Market Analysis: Unexpected Weakness Emerges

The U.S. labor market, which has been remarkably resilient in the face of aggressive monetary tightening, is finally showing significant signs of cooling. The Bureau of Labor Statistics reported that total nonfarm payroll employment unexpectedly fell by 92,000 jobs in February 2026. This decline was a stark contrast to consensus expectations, which had anticipated a modest gain of roughly 50,000 jobs, and follows a downwardly revised increase of 126,000 jobs in January.

Accompanying the drop in payrolls was an increase in the unemployment rate, which ticked up to 4.4 percent in February from 4.3 percent in the previous month. While an unemployment rate of 4.4 percent is still relatively low by historical standards, the upward trend is a clear indication that the labor market is loosening. The job losses were broad-based, with declines noted in several major industries, including manufacturing and construction, suggesting that the impact of higher interest rates is beginning to weigh heavily on corporate hiring decisions.

This unexpected weakness in the labor market complicates the Federal Reserve's dual mandate of price stability and maximum employment. While the Fed has been primarily focused on combating inflation, the sudden deterioration in employment data will undoubtedly force policymakers to carefully weigh the risks of overtightening. If job losses continue to mount in subsequent months, the Fed may be pressured to pivot toward rate cuts sooner than currently anticipated, even if inflation remains slightly above target.

Investment implications: A weakening labor market typically precedes a broader economic slowdown or recession. In this scenario, defensive sectors such as consumer staples, healthcare, and utilities tend to outperform more cyclical areas of the market. Investors should be cautious regarding consumer discretionary stocks, as rising unemployment will likely lead to reduced consumer spending. Furthermore, if the labor market deterioration accelerates, it could prompt a rally in long-term bonds as the market begins to price in future interest rate cuts by the Federal Reserve.

Growth & Consumer Indicators: A Sharp Deceleration

Economic growth in the United States has slowed dramatically, according to the latest data from the Bureau of Economic Analysis. The second estimate for real Gross Domestic Product (GDP) showed that the economy grew at an annualized rate of just 0.7 percent in the fourth quarter of 2025. This represents a significant downward revision from previous estimates and a sharp deceleration from the robust growth seen earlier in the year. The slowdown in GDP growth was primarily driven by a deceleration in consumer spending, a downturn in private inventory investment, and a decrease in nonresidential fixed investment.

Despite the sharp drop in overall economic growth, consumer spending—which accounts for more than two-thirds of U.S. economic activity—has shown mixed signals. While the GDP report indicated a slowdown in consumption, recent retail sales data suggests that consumers are still spending, albeit at a more moderate pace. Retail sales grew by 0.28 percent month-over-month in February 2026, and were up a solid 6.24 percent year-over-year. This resilience in consumer spending is likely supported by previous wage gains, although the recent weakening in the labor market poses a significant threat to future consumption.

Looking ahead, the outlook for economic growth remains highly uncertain. The combination of restrictive monetary policy, a cooling labor market, and depleted consumer savings suggests that the economy will continue to face significant headwinds in the first half of 2026. Many economists and market analysts are increasingly raising the odds of a mild recession occurring later in the year if current trends persist.

Investment implications: The sharp deceleration in GDP growth underscores the need for a cautious approach to equity markets. Investors should focus on high-quality companies with strong balance sheets, consistent cash flows, and sustainable dividend yields. Small-cap stocks and companies highly sensitive to economic cycles may face significant challenges in a low-growth environment. Conversely, a slowing economy could provide a supportive backdrop for high-quality fixed-income investments, as slowing growth typically leads to lower bond yields and higher bond prices.

Market Implications & Outlook: Navigating the Crosscurrents

The current economic data presents a challenging environment for financial markets. The combination of sticky inflation, a weakening labor market, and sharply decelerating economic growth creates a scenario that is difficult for both equity and fixed-income investors to navigate. The Federal Reserve's commitment to holding interest rates steady at 3.50 to 3.75 percent, despite the emerging weakness in employment and GDP, suggests that policymakers are willing to risk a mild recession to ensure that inflation is fully vanquished.

For the stock market, this environment implies continued volatility. Equity valuations, particularly in the technology and growth sectors, remain relatively high and may be vulnerable to a correction if corporate earnings begin to disappoint due to slowing economic activity. However, the market is also forward-looking, and any signs that inflation is finally breaking could lead to a rapid repricing of assets in anticipation of future rate cuts.

Ultimately, the key to successful investing in this environment is diversification and a focus on quality. Investors should avoid making outsized bets on a single macroeconomic outcome and instead build portfolios that can withstand a range of scenarios. By carefully monitoring incoming data on inflation, employment, and consumer spending, investors can adjust their strategies to navigate the complex crosscurrents of the 2026 economy.

Disclaimer: This analysis is for informational and educational purposes only and should not be considered financial advice. Economic forecasts are subject to significant uncertainty and actual results may differ materially. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.