Stock Introduction & Thesis

NVIDIA Corporation (NASDAQ: NVDA) has firmly established itself as the undisputed leader in the artificial intelligence revolution, transforming from a graphics processing unit (GPU) pioneer into the foundational infrastructure provider for the modern computing era. With a market capitalization hovering around $4.8 trillion, NVIDIA commands an estimated 90% share of the AI accelerator market. The company's core business model revolves around designing and selling high-performance GPUs, networking equipment, and comprehensive software platforms that power data centers, enterprise AI applications, and advanced research facilities worldwide.

The investment thesis for NVIDIA centers on its impenetrable competitive moat, which is built not just on superior hardware like the current Blackwell architecture and the upcoming Vera Rubin platform, but on its proprietary CUDA software ecosystem. This software layer has locked in millions of developers, making it exceptionally difficult for competitors to displace NVIDIA's hardware. As the technology sector undergoes a structural shift from traditional computing to generative and agentic AI, NVIDIA stands as the primary beneficiary. The company is effectively selling the “picks and shovels” for the AI gold rush, positioning it for sustained, multi-year growth as hyperscalers and enterprises alike race to build out their AI infrastructure.

Recent Developments & Catalysts

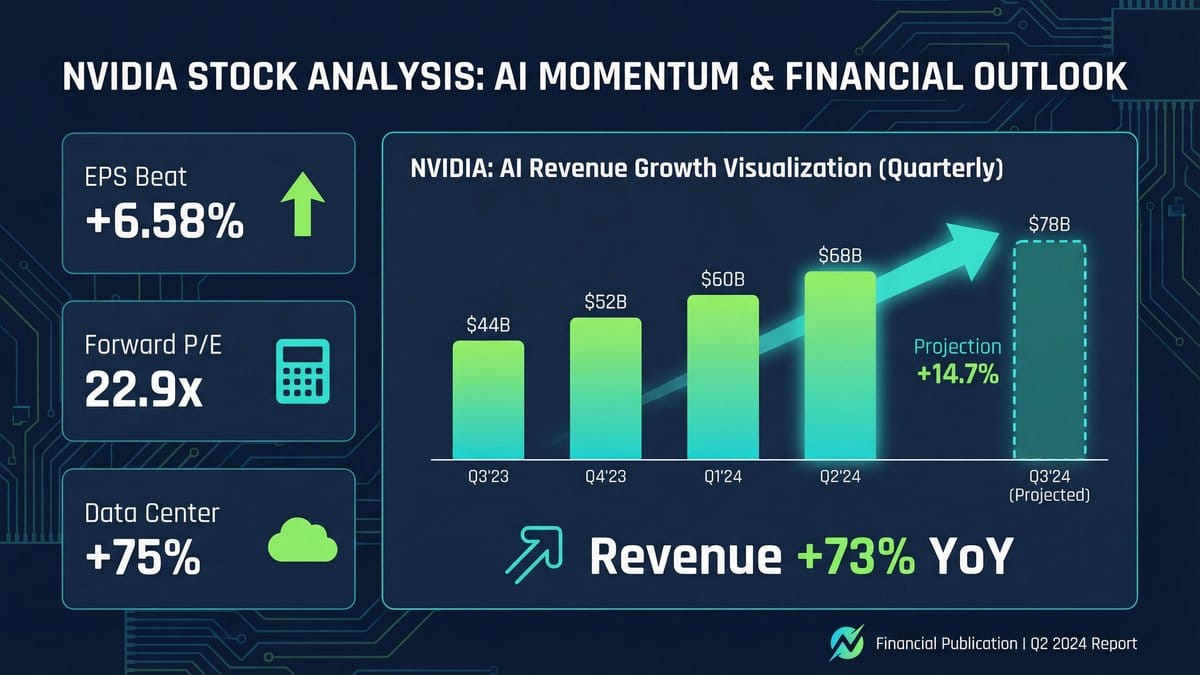

NVIDIA's recent fiscal fourth-quarter 2026 earnings report, released in late February, shattered even the most optimistic Wall Street expectations. The company reported record revenue of $68.13 billion for the quarter, representing a staggering 73.2% year-over-year increase and a 20% sequential jump from the third quarter. This performance was driven almost entirely by the Data Center segment, which alone generated $62.31 billion, up 75% year-over-year. Non-GAAP earnings per share came in at $1.62, beating the consensus estimate of $1.52 by 6.58%.

Beyond the raw numbers, the most significant recent catalyst is the ongoing GTC 2026 conference, running March 16–19 in San Jose, California. During his keynote, CEO Jensen Huang outlined a breathtaking $1 trillion revenue opportunity for AI chips through 2027. The company also unveiled the Groq 3 AI chip and CPU server, directly targeting Intel's market share, and provided deeper insights into the Vera Rubin next-generation architecture. Furthermore, NVIDIA's networking revenue surged 263% year-over-year to $10.98 billion, highlighting the massive adoption of its NVLink fabric for large-scale AI systems. Looking ahead, management guided for Q1 fiscal 2027 revenue of approximately $78.0 billion, signaling that the exponential demand curve shows no signs of flattening.

Investment implications: The sheer magnitude of NVIDIA's revenue beat and forward guidance completely invalidates near-term concerns about an “AI bubble” bursting. The $1 trillion revenue forecast through 2027 provides unprecedented visibility into future cash flows, suggesting that the current capital expenditure cycle by major cloud providers is not a temporary spike, but a sustained, multi-year infrastructure buildout. Investors should view these developments as confirmation that NVIDIA's growth trajectory remains robust and deeply entrenched in global enterprise spending plans.

Financial Analysis

A deep dive into NVIDIA's financial metrics reveals a company operating with unprecedented efficiency and scale. For the full fiscal year 2026, total revenue reached $215.94 billion, a 65.47% increase from the $130.5 billion reported in fiscal 2025. This growth is even more remarkable when considering the base effect; NVIDIA is adding tens of billions of dollars in new revenue each quarter. The quarterly progression throughout fiscal 2026 illustrates this momentum perfectly: $44.1 billion in Q1, $46.7 billion in Q2, $57.0 billion in Q3, and culminating in the $68.1 billion Q4 print.

Profitability metrics are equally impressive. The company's GAAP gross margin expanded to 75.0% in Q4, up from 73.4% in the previous quarter, while non-GAAP gross margin hit 75.2%. This margin expansion, occurring simultaneously with massive revenue growth, demonstrates incredible pricing power and operational leverage. GAAP net income for the full year stood at $120.1 billion, translating to a non-GAAP EPS of $4.77. Furthermore, NVIDIA generated a massive $34.90 billion in free cash flow just in the fourth quarter, providing the company with an enormous war chest for research and development, strategic acquisitions, and shareholder returns.

Investment implications: NVIDIA's financial profile is arguably the strongest of any mega-cap technology company in history. The combination of 70%+ revenue growth and 75%+ gross margins is exceptionally rare and indicates a near-monopoly position with immense pricing power. The massive free cash flow generation ensures that NVIDIA can outspend any competitor on R&D to maintain its technological lead, while simultaneously returning capital to shareholders. This financial fortress significantly de-risks the investment from a fundamental perspective.

Valuation & Competitive Position

Despite its astronomical run over the past three years, NVIDIA's valuation remains surprisingly reasonable when viewed through the lens of its growth rate. As of mid-March 2026, the stock trades at a trailing P/E ratio of approximately 37.7x. However, because earnings are growing so rapidly, the forward P/E ratio drops to roughly 22.9x, which is actually below the semiconductor sector average of 29.14x. When factoring in the expected 60% earnings growth for the current fiscal year, NVIDIA's Price-to-Earnings-to-Growth (PEG) ratio sits at an incredibly attractive 0.58x. A PEG ratio below 1.0 is traditionally considered an indicator of an undervalued stock relative to its growth potential.

Competitively, NVIDIA operates in a league of its own. While Advanced Micro Devices (AMD) is making strides with its MI300X accelerators, and hyperscalers like Google, Amazon, and Microsoft are developing custom silicon (TPUs, Trainium, Maia), none pose an immediate existential threat to NVIDIA's dominance. NVIDIA's competitive advantage is not just the silicon; it is the entire system architecture. The combination of industry-leading GPUs, the NVLink networking fabric that ties them together, and the ubiquitous CUDA software platform creates a sticky ecosystem that is prohibitively expensive and complex for customers to abandon.

Investment implications: The market is currently pricing NVIDIA as a mature, slower-growth company based on its forward P/E of 22.9x, completely ignoring the massive growth implied by its 0.58x PEG ratio. This presents a compelling opportunity for investors. The stock is not overvalued; rather, the market is underestimating the durability and magnitude of the AI infrastructure buildout. Given its impenetrable competitive moat and reasonable forward valuation, NVIDIA remains a core holding for any growth-oriented portfolio.

Risks & Outlook

While the bull case for NVIDIA is overwhelmingly strong, several key risks must be monitored. Geopolitical tensions, specifically regarding U.S. export restrictions to China, remain a persistent headwind. Management's Q1 fiscal 2027 guidance of $78 billion explicitly excludes any Data Center compute revenue from China, indicating that the company has already factored this loss into its projections, but further regulatory tightening could still impact global supply chains. Additionally, customer concentration is a significant risk; a large portion of NVIDIA's revenue comes from a handful of hyperscalers (Amazon, Meta, Microsoft, Alphabet). If these companies were to suddenly pull back on capital expenditures, NVIDIA's revenue would take an immediate hit.

Looking ahead, the outlook remains exceptionally bright. The transition from generative AI to “agentic AI”—systems that can autonomously perform complex, multi-step tasks—will require an order of magnitude more computing power. CEO Jensen Huang has correctly noted that in the AI era, “compute is revenues.” As long as enterprises continue to see a return on investment from AI deployments, the demand for NVIDIA's hardware and software will persist. The upcoming rollout of the Vera Rubin architecture and the continued expansion of the networking business provide clear catalysts for sustained growth through the end of the decade.

Disclaimer: This analysis is for informational and educational purposes only and should not be considered financial advice. Individual stock investments carry significant risks including company-specific and market risks. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.