Arista Networks: The Hidden Engine Powering the AI Revolution

While semiconductor giants often dominate the headlines surrounding artificial intelligence, the massive data centers required to train and run these models rely on an equally critical component: high-speed networking. Arista Networks (NYSE: ANET) has emerged as the premier provider of cloud networking solutions, positioning itself as an indispensable player in the AI infrastructure buildout. The company specializes in designing and selling multilayer network switches to deliver software-defined networking for large-scale data centers, cloud computing environments, and high-performance computing clusters.

The core investment thesis for Arista Networks centers on its dominant competitive position in the “Hyperscale AI Innovator” customer segment. As AI workloads put unprecedented pressure on front-end cloud infrastructure and require massive back-end network deployments to connect GPU clusters, the demand for high-bandwidth, low-latency Ethernet networking is surging. Arista's Extensible Operating System (EOS) and its hardware-agnostic approach provide a significant competitive moat, allowing the company to capture market share from legacy providers while maintaining exceptional profitability.

Recent Developments & Catalysts

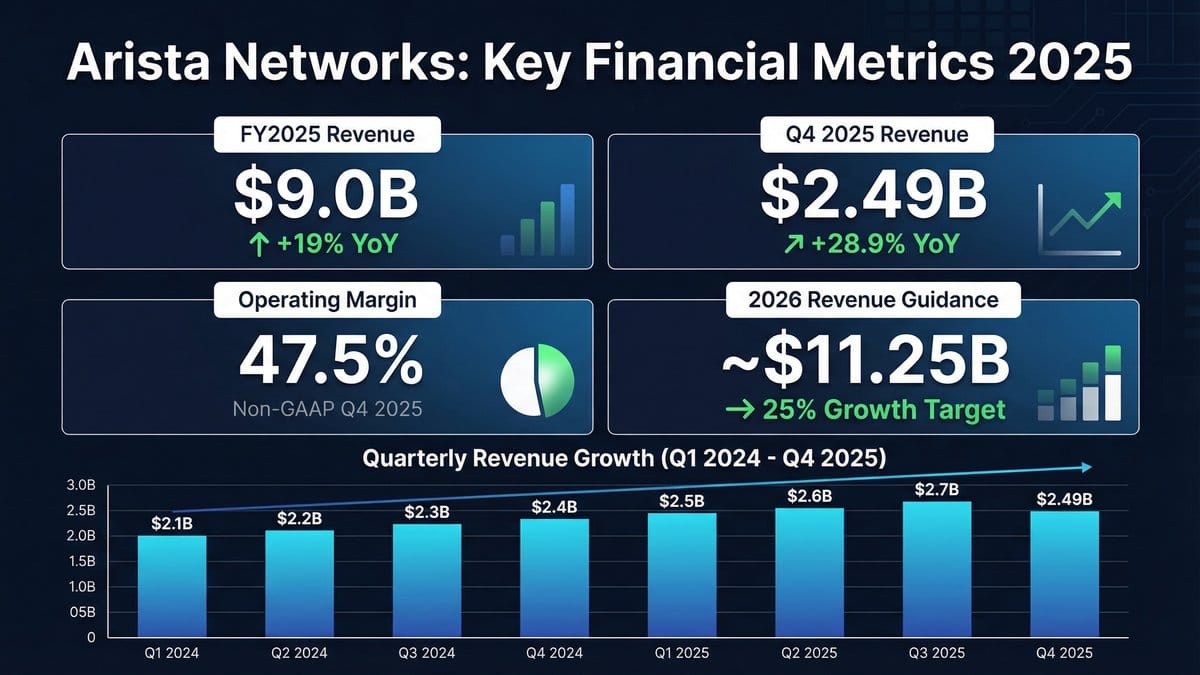

Arista Networks recently delivered a stellar fourth-quarter 2025 earnings report that significantly exceeded Wall Street expectations. The company reported an EPS of $0.82, beating the consensus estimate of $0.75 by $0.07. More importantly, quarterly revenue rose an impressive 28.9% year-over-year to $2.49 billion, surpassing expectations of $2.38 billion. This strong finish contributed to a remarkable fiscal year 2025, demonstrating the company's ability to execute flawlessly amid surging demand.

The most significant catalyst, however, came from management's updated forward-looking guidance. Arista significantly increased its 2026 AI networking revenue target from $2.75 billion to $3.25 billion, highlighting robust demand and “production scale” for its Ethernet solutions within AI data centers. Furthermore, the company raised its full-year 2026 revenue guidance to approximately $11.25 billion, targeting 25% growth. Management also outlined a massive expansion of its total addressable market (TAM), doubling it from $60 billion to $105 billion, driven by the rapid proliferation of AI infrastructure requirements.

Investment implications: The substantial upward revision in AI networking revenue targets and the expanded TAM indicate that Arista is not just participating in the AI boom, but accelerating its market capture. The transition to 800-gigabit Ethernet is happening faster than anticipated, and Arista is perfectly positioned to capitalize on this upgrade cycle, providing a strong catalyst for continued stock price appreciation.

Financial Analysis

Arista Networks' financial trajectory over the past several years has been nothing short of exceptional. The company's revenue has grown consistently, culminating in a record $9.0 billion for the full fiscal year 2025. This represents a massive acceleration from previous years, driven by the hyperscale cloud titans upgrading their infrastructure to support AI workloads. The fourth quarter of 2025 alone generated $2.49 billion, showcasing the accelerating momentum in the business.

Beyond top-line growth, Arista's profitability metrics are industry-leading. The company reported a remarkable 47.5% non-GAAP operating margin in Q4 2025, translating to $1.05 billion in net income for the quarter. This high margin profile is a testament to the value proposition of Arista's software-centric approach (EOS) and its strong pricing power in a market currently experiencing a supply deficit for high-speed switching. Furthermore, Arista is a cash-generating machine, producing $4.37 billion of net cash from operating activities in 2025, up from $3.71 billion in 2024. This robust cash flow provides the company with ample resources for continued R&D investment and shareholder returns.

Investment implications: Arista's combination of hyper-growth and elite profitability is rare. The company's ability to expand margins while scaling revenue at nearly 30% year-over-year demonstrates immense operating leverage. This financial strength provides a significant margin of safety and the flexibility to navigate any potential macroeconomic headwinds while continuing to invest in next-generation technologies.

Valuation & Competitive Position

From a valuation perspective, Arista Networks trades at a premium, reflecting its high growth rate and strategic importance in the AI ecosystem. The stock currently trades at a trailing P/E ratio of approximately 49x and a forward P/E of around 44x based on 2026 estimates. While this is significantly higher than the broader market and legacy networking peers, it is arguably justified by the company's 25%+ projected revenue growth and near-50% operating margins.

Arista's competitive position is formidable. The company has successfully disrupted the traditional networking market, taking significant share from incumbents like Cisco Systems. Arista's advantage lies in its merchant silicon strategy and its highly regarded EOS software, which provides superior reliability, programmability, and automation capabilities. In the critical AI data center market, Arista is the undisputed leader in high-speed Ethernet switching, successfully defending its turf against both traditional networking rivals and vertically integrated solutions like Nvidia's InfiniBand.

Investment implications: While the valuation multiples are elevated, Arista's premium is warranted given its dominant market share in the fastest-growing segment of technology infrastructure. Investors are paying for a high-quality, wide-moat business that is a direct derivative play on the multi-year AI capital expenditure cycle. The company's strong pricing power and expanding TAM suggest that it can grow into its valuation over the next several years.

Risks & Outlook

Despite the overwhelmingly positive fundamental picture, an investment in Arista Networks is not without risks. The most prominent concern is customer concentration. Historically, a significant portion of Arista's revenue has been derived from just two major hyperscalers: Microsoft and Meta Platforms. Any slowdown, pause, or shift in capital expenditure plans by these key customers could have an outsized negative impact on Arista's financial results. However, management has recently signaled the emergence of additional 10%+ customers in 2026, which should help mitigate this concentration risk over time.

Another risk is the intense competitive landscape. While Arista currently leads in Ethernet switching for AI, it faces formidable competition from Nvidia's proprietary InfiniBand technology, which is often bundled with its highly sought-after GPUs. Additionally, legacy players like Cisco are aggressively investing to regain market share in the AI networking space. Finally, as a hardware manufacturer, Arista is exposed to supply chain vulnerabilities and potential geopolitical risks, including tariffs on components sourced from overseas.

Disclaimer: This analysis is for informational and educational purposes only and should not be considered financial advice. Individual stock investments carry significant risks including company-specific and market risks. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.