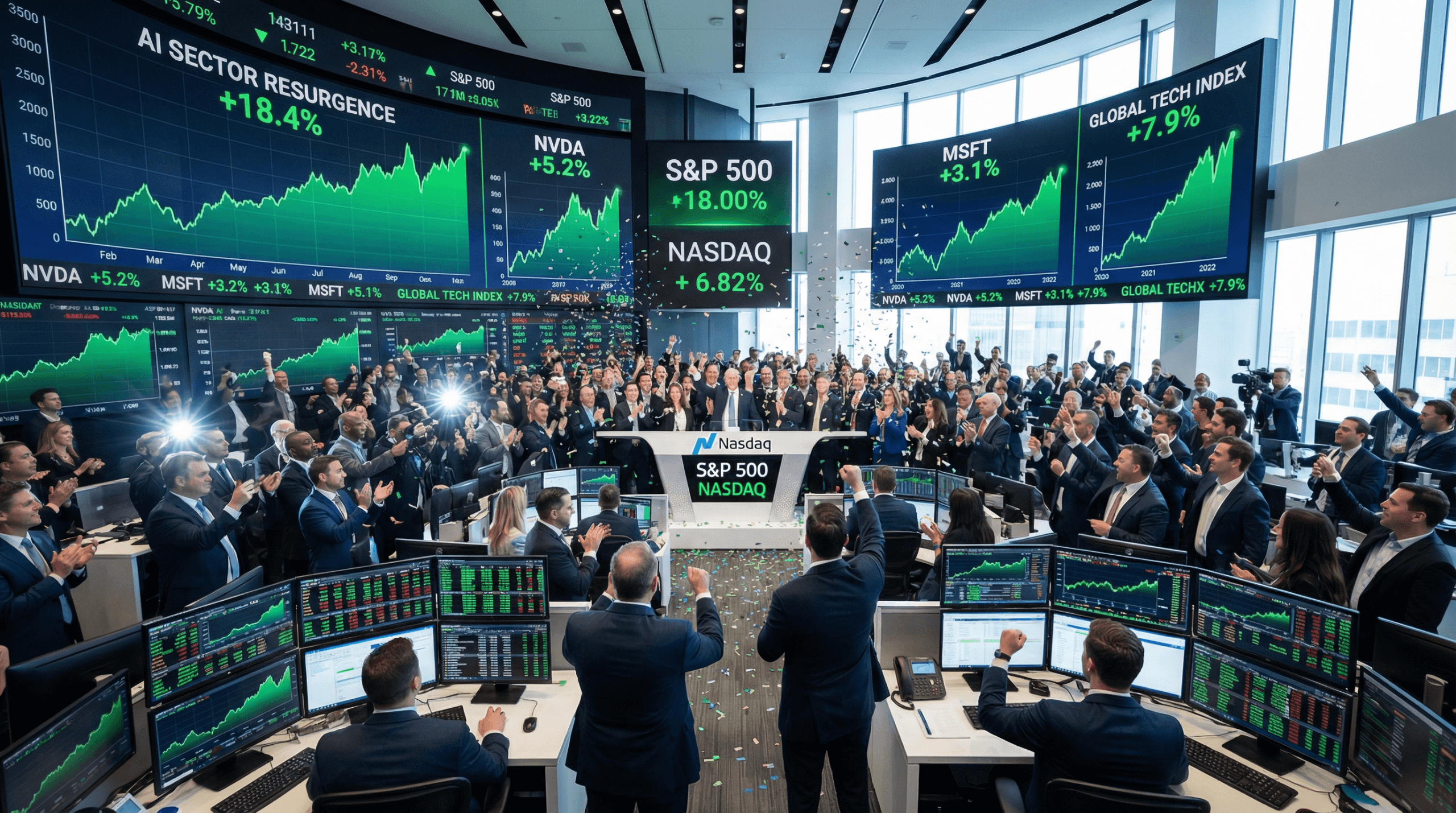

1. AI Trade Roars Back as Markets Rally for Second Straight Day, S&P 500 and Nasdaq Post Weekly Gains

Summary: U.S. stock markets surged for a second consecutive session on Friday, December 19, 2025, with artificial intelligence-related shares leading a powerful rally that erased weekly losses for the S&P 500 and Nasdaq, as the benchmark index rose 0.9% to 6,834.50, the Nasdaq Composite jumped 1.3% to 23,307.62, and the Dow Jones Industrial Average gained 0.4% to 48,134.89, marking a dramatic reversal in market sentiment as risk appetite returned following Thursday's better-than-expected inflation data. The tech-heavy Nasdaq's 1.3% Friday gain followed Thursday's 1.4% advance, allowing the index to post a 0.5% weekly gain after dropping nearly 2% on Wednesday, while the S&P 500's 0.9% Friday surge enabled it to finish up 0.1% for the week after snapping a four-session losing streak on Thursday. Chipmaker stocks led the charge with Micron Technology extending its rally with a 7% gain on top of Thursday's 10% surge, Nvidia advancing 4%, and Advanced Micro Devices climbing 6%, while Oracle jumped 6.6% on the TikTok joint venture news, validating the AI infrastructure investment thesis that had been under severe pressure in recent weeks.

Why it matters for investors: The two-day AI trade resurgence represents a critical test of whether the recent technology sector selloff was merely a healthy correction or the beginning of a more severe downturn, with Friday's broad-based rally in semiconductor and cloud infrastructure stocks suggesting that investor appetite for AI exposure remains intact despite concerns about capital expenditure sustainability and valuation multiples that had driven the Nasdaq down nearly 2% mid-week. The fact that the S&P 500 and Nasdaq managed to post weekly gains after sharp Friday rallies—with the Nasdaq up 0.5% and S&P 500 up 0.1% for the week—demonstrates the market's resilience and willingness to buy technology dips, though the Dow's 0.7% weekly loss indicates continued rotation pressure as value-oriented investors remain skeptical of growth stock valuations. Micron's two-day gain of approximately 17-18% following its extraordinary earnings beat provides concrete validation that AI infrastructure demand remains robust, directly challenging the “AI bubble” narrative and suggesting that memory and storage bottlenecks could make certain semiconductor segments more attractive than GPU makers facing intensifying competition. However, investors must recognize that the rally occurred during quadruple witching week with over $7.1 trillion in notional options exposure expiring, creating technical volatility that may not reflect genuine shifts in fundamental sentiment, while the year-to-date performance showing Nasdaq up more than 20%, S&P 500 up 16%, and Dow up 13% suggests the market has already priced in substantial optimism about AI-driven productivity gains and may be vulnerable to disappointment if 2026 earnings fail to meet elevated expectations.

2. Bank of Japan Raises Rates to 30-Year High, Triggering Global Bond Market Volatility

Summary: The Bank of Japan delivered a historic monetary policy shift on Friday, December 19, 2025, raising interest rates to their highest level in 30 years in a move that sent ripples through global bond markets and pushed the U.S. 10-year Treasury yield to 4.15% from Thursday's close of 4.12%, marking a significant departure from the ultra-loose monetary policy that has characterized Japanese central banking for decades. The rate hike represents the BOJ's most aggressive tightening stance since the mid-1990s and signals growing confidence among Japanese policymakers that inflation has become sustainably embedded in the economy, allowing them to normalize monetary policy after years of fighting deflation with negative interest rates and massive quantitative easing programs. The decision comes as BOJ Governor Kazuo Ueda has repeatedly signaled the central bank's intention to continue raising rates in 2026, with the 10-year Japanese Government Bond yield having already hit a 26-year high in recent sessions, creating a dramatic shift in the global interest rate landscape as one of the world's largest economies moves from extreme accommodation to gradual tightening.

Why it matters for investors: The Bank of Japan's rate hike to a 30-year high represents a seismic shift in global monetary policy dynamics that could have far-reaching implications for currency markets, international capital flows, and asset valuations across multiple regions, as Japanese investors who have been forced to seek returns overseas due to negative domestic rates may now find attractive opportunities at home, potentially triggering repatriation flows that could strengthen the yen and put pressure on U.S. Treasuries, equities, and other assets that have benefited from Japanese capital inflows. The immediate impact on U.S. Treasury yields—with the 10-year rising to 4.15% from 4.12%—may seem modest but signals the beginning of a structural shift where global interest rates face upward pressure not just from Federal Reserve policy but from synchronized tightening by major central banks, creating a more challenging environment for highly leveraged companies, growth stocks trading at elevated multiples, and real estate assets that have thrived in the ultra-low rate environment of the past decade. The BOJ's move contrasts sharply with the Federal Reserve's recent signal of only one more rate cut in 2026 and the European Central Bank's decision to hold rates steady while upgrading growth forecasts, suggesting that global monetary policy is entering a new phase where central banks are less coordinated and more focused on domestic inflation dynamics, creating potential for currency volatility and cross-border capital flow disruptions that could amplify market swings. For portfolio construction, the BOJ's historic rate hike argues for increased attention to currency hedging strategies, reduced exposure to yen-carry trades that have been popular for years, and careful assessment of which assets are most vulnerable to Japanese capital repatriation, while also creating potential opportunities in Japanese equities and bonds that may become more attractive to domestic investors as the yield differential with overseas markets narrows.

3. Major Pharmaceutical Companies Agree to $150 Billion Manufacturing Investment and Drug Price Cuts Under Trump Pressure

Summary: In a landmark deal announced Friday, December 19, 2025, several major pharmaceutical companies including Amgen, Bristol Myers Squibb, Gilead Sciences, GSK, Merck, Novartis, and Sanofi agreed to lower prescription drug prices for Americans to match the lowest prices paid by other developed nations—known as most-favored-nation pricing—while committing to invest at least $150 billion collectively in U.S. manufacturing in the near term, with shares of these companies rising 1% to 3.5% as investors welcomed the deal that allows them to avoid President Trump's planned pharmaceutical tariffs for three years. The agreement, which also includes privately held German company Boehringer Ingelheim and Genentech (a unit of Swiss firm Roche), represents a major policy victory for the Trump administration's efforts to reduce healthcare costs for Americans while simultaneously reshoring pharmaceutical manufacturing capacity that has increasingly shifted to China and other overseas locations in recent decades. The White House framed the deal as a win-win that addresses both the affordability crisis facing American consumers struggling with high drug costs and the national security concerns about over-reliance on foreign pharmaceutical supply chains, with the $150 billion manufacturing investment commitment representing one of the largest industrial policy initiatives in the healthcare sector's history.

Why it matters for investors: The pharmaceutical industry's capitulation to Trump administration pressure on drug pricing and manufacturing represents a watershed moment that fundamentally alters the sector's economics and strategic priorities, with the agreement to adopt most-favored-nation pricing potentially compressing profit margins on drugs sold in the U.S. market while the $150 billion manufacturing investment commitment will require significant capital reallocation away from share buybacks, dividends, or research spending toward building domestic production capacity. The market's positive initial reaction—with pharmaceutical stocks rising 1% to 3.5%—suggests investors view the three-year tariff exemption and regulatory certainty as more valuable than the revenue headwinds from lower drug prices, but this assessment may prove optimistic if the most-favored-nation pricing mechanism results in steeper price cuts than companies currently anticipate, particularly for blockbuster drugs where U.S. prices are multiples of what other developed nations pay. The $150 billion manufacturing investment commitment, while spread across multiple companies and described as “near term” without specific timeline details, represents a massive capital deployment that will take years to fully implement and may face challenges including labor shortages, permitting delays, and the reality that pharmaceutical manufacturing is a complex, highly regulated process that cannot be easily reshored without significant disruption to existing supply chains. For sector investors, the deal creates a bifurcated outlook where companies with strong pipeline assets and diversified geographic revenue streams may weather the pricing pressure better than those heavily dependent on U.S. sales of mature products, while the manufacturing investment requirement may paradoxically benefit pharmaceutical equipment suppliers, construction companies, and specialized contractors who will be needed to build out the new domestic production capacity, creating a potential investment opportunity in the picks-and-shovels companies serving the pharmaceutical reshoring trend.

4. Oracle and Micron Lead Semiconductor Rally, Validating AI Infrastructure Demand Thesis

Summary: Semiconductor and cloud infrastructure stocks staged a powerful two-day rally on December 18-19, 2025, with Oracle shares surging 6.6% on Friday following reports that China's ByteDance is creating a joint venture granting American investors including the cloud computing giant a controlling stake in TikTok, while Micron Technology extended its extraordinary rally with a 7% Friday gain on top of Thursday's 10% surge after posting earnings that dramatically exceeded expectations with revenue guidance of $18.70 billion versus $14.20 billion expected. The semiconductor rally broadened beyond these two standout performers, with Nvidia advancing approximately 4% and Advanced Micro Devices climbing 6% on Friday, suggesting that investor confidence in the artificial intelligence infrastructure buildout is returning after weeks of skepticism about capital expenditure sustainability and concerns about an AI bubble that had hammered technology stocks and pushed Oracle down 45% from its September all-time high. Micron's assertion that it is “more than sold out” with “significant unmet demand” for high-bandwidth memory products and its projection that the total addressable market will reach $100 billion by 2028 with a 40% compound annual growth rate provided concrete evidence that contradicts the AI bubble narrative, while Oracle's TikTok deal guarantees a massive cloud infrastructure customer and provides upside optionality from the social media platform's growth trajectory.

Why it matters for investors: The synchronized rally in Oracle and Micron—two companies that had become poster children for investor skepticism about AI infrastructure spending—represents a potential inflection point for the semiconductor sector and could signal that the recent selloff was a healthy correction rather than the beginning of a prolonged downturn, with Micron's extraordinary 32% revenue guidance beat based on actual customer commitments rather than speculative projections providing the most compelling evidence yet that hyperscale cloud providers and enterprise customers remain committed to massive AI infrastructure investments. Oracle's TikTok joint venture deal is particularly significant because it transforms the company from merely a service provider into a core equity holder with direct exposure to TikTok's growth and advertising economics, while also providing access to sophisticated AI and recommendation algorithms that could enhance Oracle's own product offerings, potentially justifying a valuation re-rating if the company can demonstrate that the deal materially improves its competitive position against Amazon Web Services, Microsoft Azure, and Google Cloud. However, investors must carefully assess whether this two-day rally represents a genuine reversal or merely a relief bounce in stocks that remain deeply oversold, with Oracle still down approximately 31% year-to-date despite the recent gains and questions persisting about how the company will finance the massive data center buildout required to compete with hyperscale providers, while Micron's decision to increase capital expenditure guidance to $20 billion from $18 billion raises concerns about whether the industry is entering a period of capacity expansion that could eventually lead to the oversupply and pricing pressure that has historically plagued the cyclical semiconductor memory market. The broader semiconductor rally with Nvidia up 4% and AMD up 6% suggests positive sentiment spillover across the AI supply chain, but the fact that these gains merely recovered a portion of recent losses rather than pushing stocks to new highs indicates the market remains cautious about the sector's near-term prospects, making stock selection and careful attention to valuation multiples more critical than broad-based sector exposure as we head into 2026.

5. Nike Plunges Over 10% as China Collapse and Tariff Pressures Overshadow Earnings Beat

Summary: Nike shares tumbled more than 10% on Friday, December 19, 2025, extending Thursday's after-hours decline despite the athletic apparel giant reporting fiscal second-quarter earnings and revenue that topped Wall Street estimates, as investors fixated on the company's warning of an anticipated current-quarter sales decline driven by severe headwinds in China where revenue plunged 17% to $1.42 billion and the sustained impact of higher tariffs that are eroding profitability even as North America sales rose a solid 9% to $5.63 billion. The company reported adjusted earnings of 53 cents per share versus 38 cents expected and revenue of $12.43 billion versus $12.22 billion expected, but the stark geographic divergence in performance—with strength in the home market offset by collapse in the world's second-largest economy—exposed Nike's vulnerability to geopolitical tensions, shifting Chinese consumer preferences away from Western brands, and mounting tariff pressures that represent roughly $1.5 billion in annual costs. CEO Elliott Hill, the legendary leader brought back in September 2024 to engineer a turnaround, acknowledged that the business is “midway through” a transformation that is “going to take time,” but investors clearly lack patience as the stock has now fallen approximately 20% since Hill's return was announced and roughly 30% from recent peaks, making Nike one of the worst-performing mega-cap consumer stocks despite its iconic brand and market-leading position.

Why it matters for investors: Nike's 10% plunge despite beating earnings estimates delivers a stark warning about the risks facing consumer discretionary stocks and multinational corporations with significant China exposure, as the 17% revenue collapse in Greater China suggests a fundamental deterioration in the company's competitive position that cannot be easily reversed through marketing campaigns or product innovation, with Chinese consumers increasingly favoring domestic brands like Li-Ning and Anta over Western labels amid rising nationalism and economic uncertainty. The geographic divergence—with North America up 9% while China down 17%—illustrates how U.S.-China economic decoupling is creating winners and losers even within a single company's portfolio, forcing investors to reassess the value proposition of global diversification when key markets can deteriorate rapidly due to factors beyond management control, including trade tensions, shifting consumer sentiment, and government policies that explicitly or implicitly favor domestic champions over foreign competitors. The $1.5 billion annual tariff burden mentioned in the earnings release represents a structural headwind that will persist regardless of Nike's operational execution, as the company faces a difficult choice between absorbing the costs and accepting lower margins or passing them through to consumers and risking market share losses to competitors who may have more favorable supply chain configurations or lower cost structures. For portfolio construction, Nike's collapse despite solid North America performance and an earnings beat signals that investors should approach consumer discretionary stocks with extreme caution, particularly those with significant international exposure or tariff sensitivity, as the market is clearly prioritizing forward-looking risks over backward-looking results in an environment where the traditional playbook of global brand expansion and supply chain optimization is being disrupted by geopolitical fragmentation, trade policy volatility, and the rise of nationalist consumer sentiment that favors domestic brands over multinational corporations regardless of product quality or brand heritage.