The global energy sector ended September 2025 in a precarious balance, with a growing supply glut threatening to push prices lower despite persistent geopolitical risks. While OPEC+ continued to unwind its production cuts and US output surged to record highs, a weakening demand outlook kept a lid on any significant price rallies. This delicate equilibrium has left investors and analysts closely watching for any signs of a market shift.

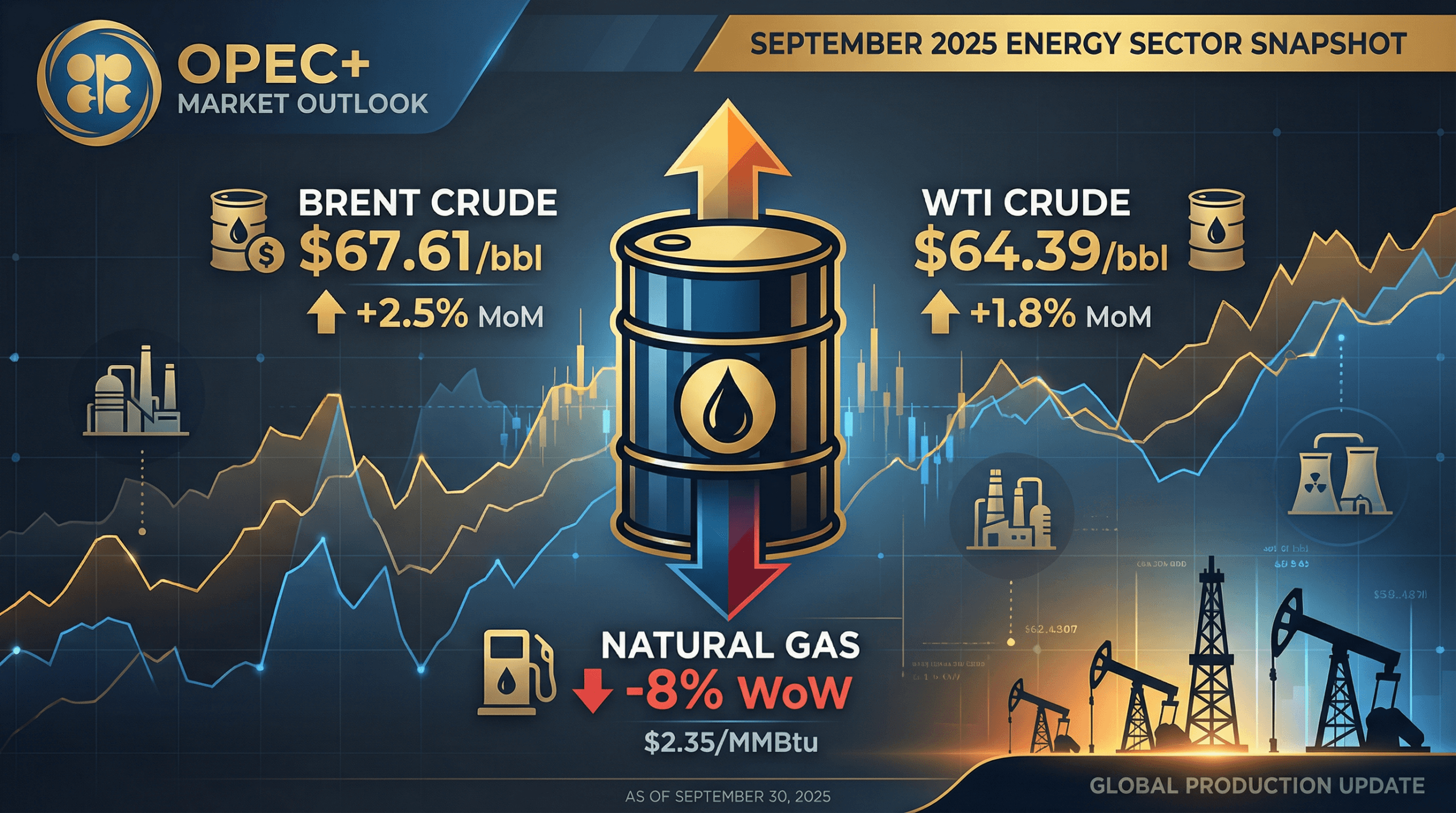

Key Weekly Energy Market Metrics

| Metric | Price | Weekly Change |

|---|---|---|

| WTI Crude Oil | $64.39/bbl | -2.1% |

| Brent Crude Oil | $67.61/bbl | -1.8% |

| Natural Gas | $2.35/MMBtu | -8.0% |

| Energy Sector ETF (XLE) | $85.50 | -1.5% |

Supply Glut Intensifies as US Production Hits Record Highs

The most significant development in September was the surge in US oil production, which reached a historic peak of 13.84 million barrels per day. This record-breaking output, coupled with OPEC+'s decision to increase production by another 137,000 barrels per day starting in October, has intensified concerns of a global supply glut. The International Energy Agency (IEA) warned that the surplus could expand in 2026 as both OPEC+ and non-OPEC+ producers ramp up output.

The growing inventories have led the US Energy Information Administration (EIA) to project a decrease in oil prices to an average of $59/bbl in the fourth quarter of 2025. This oversupply dynamic is creating a fundamentally weak market, with the balance clearly tipping toward excess supply, as visualized in the market report infographic.

Demand Outlook Weakens Amid Economic Concerns

On the other side of the equation, the demand outlook remains tepid. Analysts forecast demand to grow by a modest 0.7 million barrels per day this year, with weak economic growth and ongoing trade tariffs weighing on consumption. The slowdown in industrial activity and concerns of a global economic deceleration are further dampening demand expectations, creating a challenging environment for energy prices.

Natural gas prices have also been under pressure, falling nearly 8% week-over-week in late September. For consumers, this has translated to lower gasoline prices, with the national average for a gallon of regular dropping to $3.15.

Geopolitical Risks Provide a Floor for Prices

Despite the bearish supply-demand fundamentals, geopolitical risks are providing a floor for oil prices. Uncertainty over Russian exports remains a key factor, with Moscow introducing a partial ban on diesel exports and extending a ban on gasoline exports following a series of Ukrainian drone attacks on Russian refineries. While analysts do not expect these geopolitical tensions to cause a sustained price rally, they are preventing a complete collapse in prices.

Looking Ahead: A Market in Flux

The energy sector enters the fourth quarter of 2025 in a state of flux. The battle between a fundamentally weak, oversupplied market and the constant threat of geopolitical disruptions will continue to shape price action. Investors will be closely watching for any changes in OPEC+ policy, further developments in Russia, and any signs of a rebound in global demand. For now, the path of least resistance appears to be downward, but as always in the energy markets, volatility is the only certainty.