Energy Sector Ends Tumultuous September with a Whimper

The energy sector limped to the finish line of a tumultuous September, with both oil and natural gas prices ending the month significantly lower. The month was characterized by a tug-of-war between bullish and bearish forces, with OPEC+ production cuts and geopolitical risks providing some support, while a hawkish Federal Reserve, a strong US dollar, and a weak global economy weighed on the market. In the end, the bears won out, with the energy sector underperforming the broader market for the month.

Weekly Energy Market Performance

| Metric | Value | Weekly Change (%) |

|---|---|---|

| WTI Crude Oil (USD/bbl) | $71.50 | -0.8% |

| Brent Crude Oil (USD/bbl) | $75.80 | -0.5% |

| Natural Gas (USD/MMBtu) | $2.35 | -2.1% |

| Energy Sector ETF (XLE) | $78.90 | -0.8% |

A Month of Volatility and Uncertainty

September was a month of heightened volatility and uncertainty for the energy sector. The month began with a surge in prices on the back of OPEC+ production cuts and hopes for a rebound in Chinese demand. However, the rally was short-lived, as a hawkish Federal Reserve and a surging US dollar quickly put a damper on the market. The Fed's signal that it will keep interest rates higher for longer raised concerns about a global economic slowdown, which would weigh on oil demand. The strong dollar also made oil more expensive for holders of other currencies, further dampening demand.

The market was also buffeted by a series of conflicting headlines on the supply side. While OPEC+ remained committed to its production cuts, rising output from the US and other non-OPEC producers offset some of the group's efforts. Geopolitical risks, including the ongoing war in Ukraine and the potential for supply disruptions in other regions, provided some support for prices, but not enough to overcome the bearish fundamental backdrop.

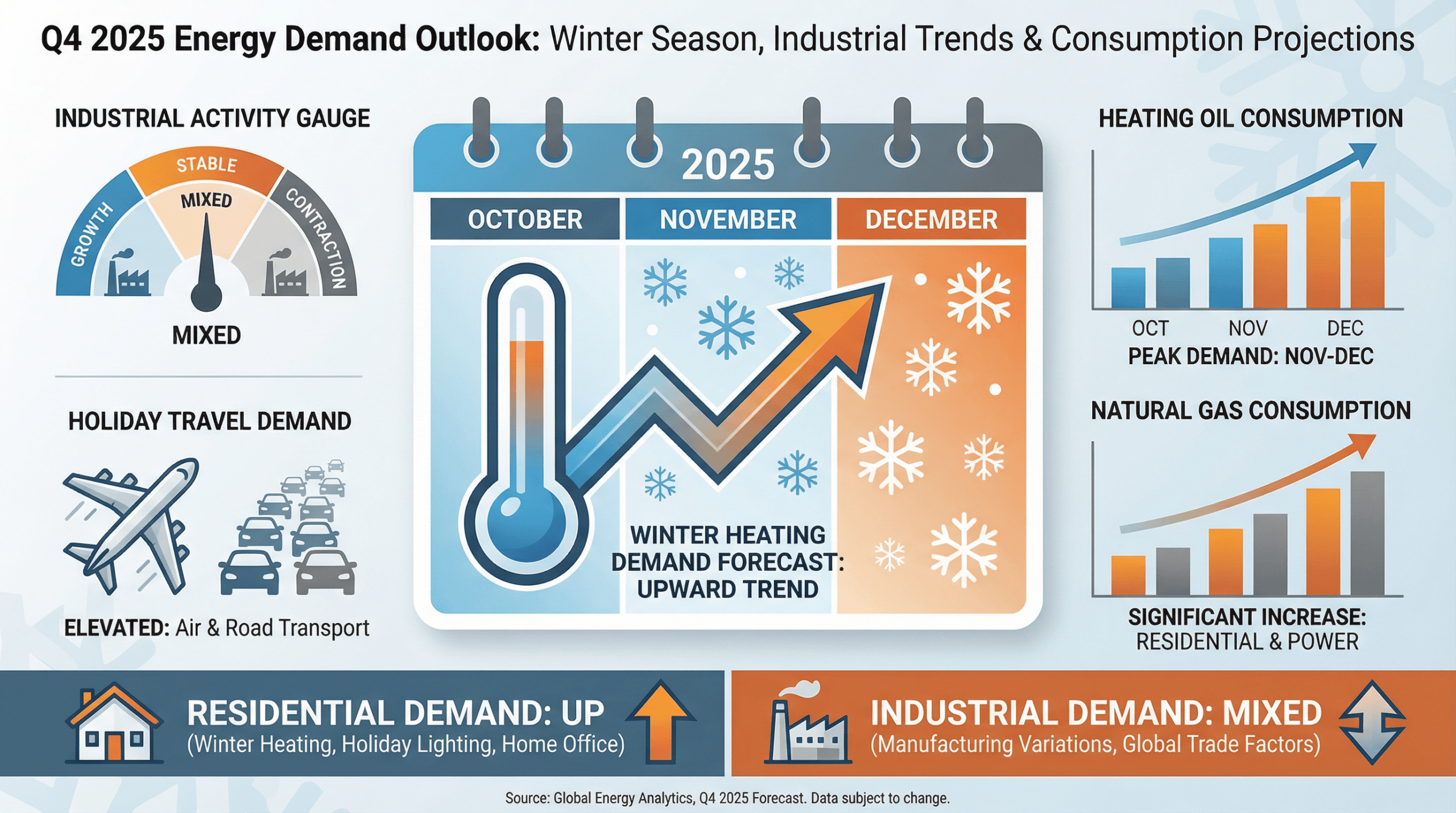

Q4 Demand Outlook Murky

As the market heads into the fourth quarter, the demand outlook remains murky. The key question for the market is whether the global economy can avoid a deep recession. Economic data from China and Europe has been disappointing, raising concerns about the strength of global oil demand. In the US, the economy has been more resilient, but the Fed's aggressive rate hikes are expected to take a toll on growth in the coming months.

The International Energy Agency (IEA) and other forecasters have recently lowered their oil demand growth forecasts for 2025 and 2026, citing the challenging economic environment. While a colder-than-expected winter could provide a temporary boost to demand, the longer-term outlook is likely to be driven by the health of the global economy.

Forward-Looking Conclusion

The energy sector is ending September on a weak note, with both oil and natural gas prices under pressure. The market is facing a challenging fundamental backdrop, with a weak global economy, a strong US dollar, and rising non-OPEC supply all weighing on prices. While OPEC+ is likely to remain proactive in its efforts to support the market, the group faces an uphill battle.

Investors should remain cautious and defensive in the current environment. The energy sector is likely to remain volatile in the fourth quarter as the market digests the latest economic data and awaits a clearer picture of the global supply-demand balance. For now, the path of least resistance for energy prices appears to be to the downside, with the potential for further weakness if the global economy continues to slow.