Energy Sector Ends October on a High Note as Winter Looms

The energy sector ended October on a high note, with both oil and natural gas prices rallying on the back of a cold snap in the US and growing anticipation of a colder-than-expected winter. The market, which had been under pressure for most of the month, staged a late-month rally as investors shifted their focus from demand concerns to the potential for a surge in heating demand. The rally was a welcome relief for energy investors, who have had to endure a volatile and challenging month.

Weekly Energy Market Performance

| Metric | Value | Weekly Change (%) |

|---|---|---|

| WTI Crude Oil (USD/bbl) | $76.20 | +3.7% |

| Brent Crude Oil (USD/bbl) | $80.50 | +3.5% |

| Natural Gas (USD/MMBtu) | $2.60 | +6.1% |

| Energy Sector ETF (XLE) | $82.50 | +3.0% |

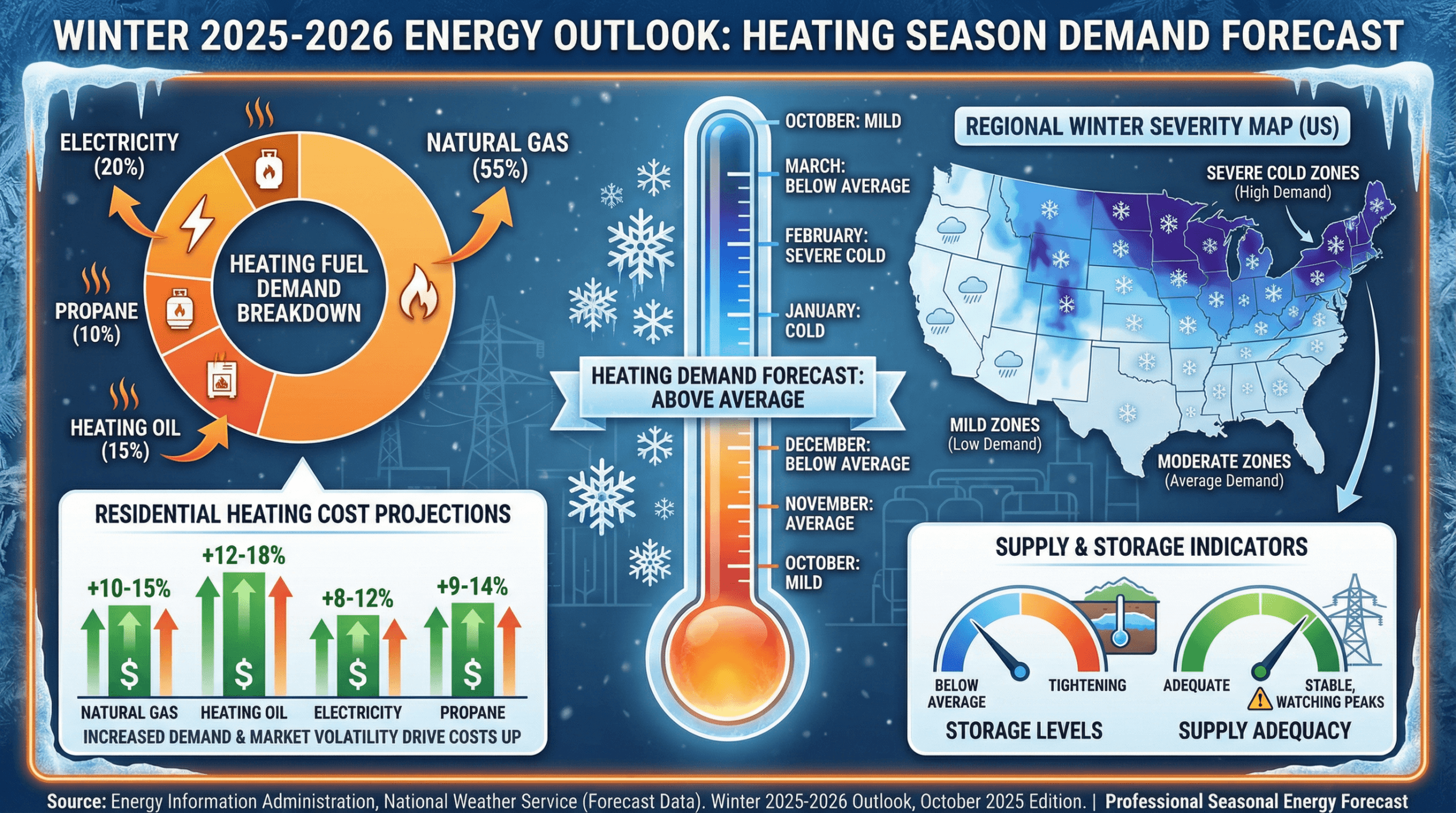

Cold Snap and Winter Outlook Boost Prices

The main driver of the energy market”s rally this week was a cold snap that swept across the US, bringing the first taste of winter to many parts of the country. The cold weather led to a surge in heating demand, which in turn boosted both natural gas and heating oil prices. The rally was further supported by forecasts for a colder-than-expected winter, which raised the prospect of a sustained increase in heating demand in the coming months.

The winter outlook is a key focus for the energy market, as it has a major impact on demand for heating fuels like natural gas and heating oil. A colder-than-expected winter can lead to a significant increase in demand, which can in turn lead to higher prices. The latest forecasts from the National Oceanic and Atmospheric Administration (NOAA) are pointing to a La Niña winter, which is typically associated with colder-than-average temperatures in the northern US. This has led many analysts to raise their price forecasts for natural gas and heating oil for the winter months.

Geopolitical Risks and OPEC+ Cuts Provide Support

Adding to the bullish sentiment were ongoing geopolitical risks and the continued commitment of OPEC+ to its production cuts. Geopolitical tensions in the Middle East remain high, and any further escalation could lead to a disruption of oil supplies. At the same time, OPEC+ has shown its willingness to be proactive in managing the market, and it is likely to take further action if prices start to fall again. The combination of geopolitical risks and OPEC+ production cuts is providing a floor for oil prices and limiting the downside potential.

Investors will be closely watching the weather forecasts in the coming weeks for clues on the winter outlook. A colder-than-expected winter could lead to a significant rally in natural gas and heating oil prices, which would in turn support the broader energy sector. However, a milder-than-expected winter could have the opposite effect, leading to a sell-off in energy prices. For now, the market is pricing in a high probability of a cold winter, which is providing a strong tailwind for the energy sector.

Forward-Looking Conclusion

The energy sector is ending October on a strong note, with both oil and natural gas prices rallying on the back of a cold snap and a bullish winter outlook. The market has shifted its focus from demand concerns to the potential for a surge in heating demand, which is providing a strong tailwind for the sector. While the market is still facing a number of headwinds, including a weak global economy and rising non-OPEC supply, the short-term outlook is bullish.

Investors should be prepared for continued volatility in the energy sector in the coming weeks as the market digests the latest weather forecasts and awaits a clearer picture of the winter outlook. The upcoming US presidential election could also be a source of volatility, as it could have a major impact on US energy policy. For now, the bulls are in control, but the bears are not far behind, waiting for any sign of a change in the narrative.