This Week's Retirement Tip

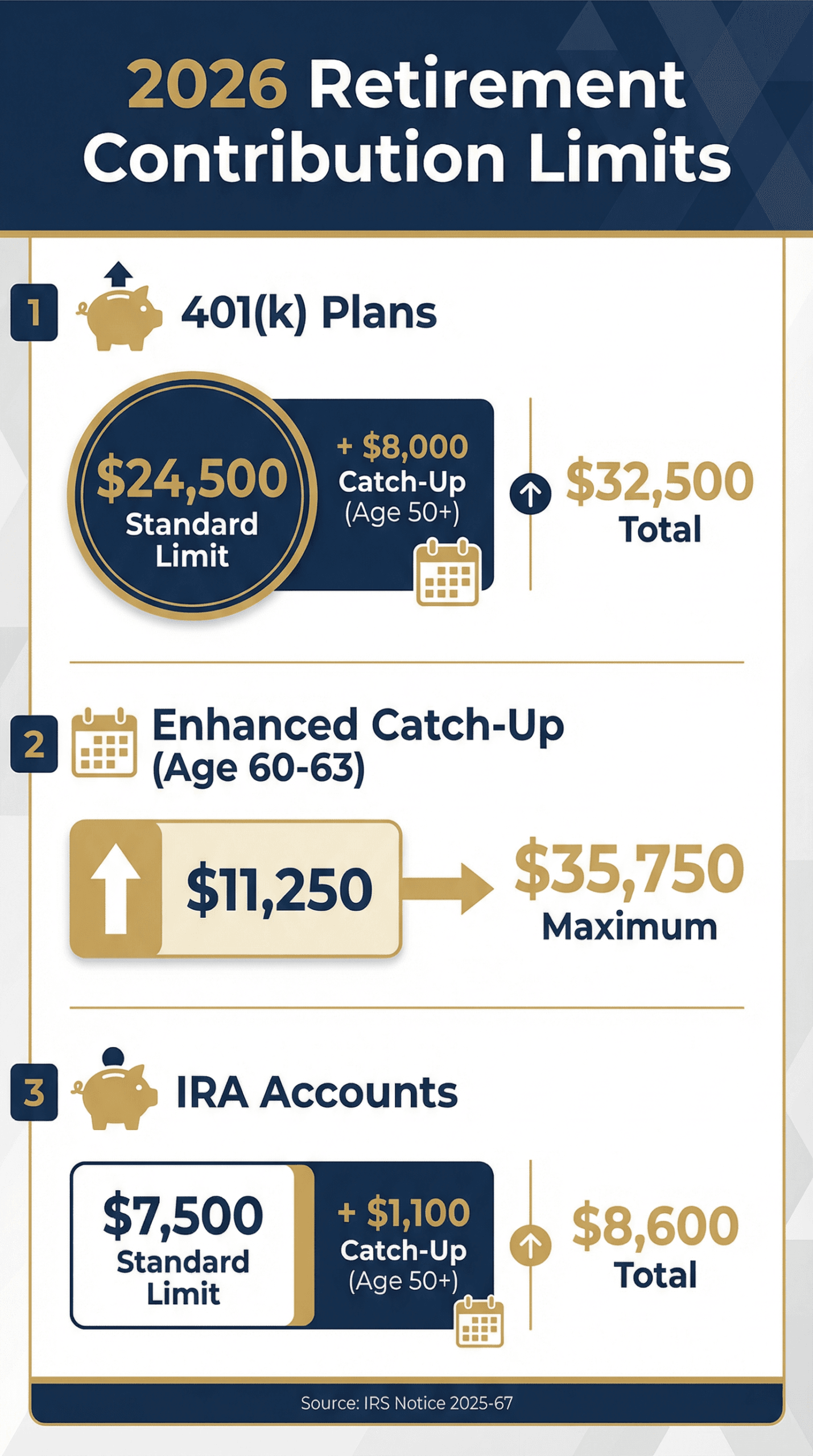

For 2026, the IRS has announced significant increases to contribution limits for retirement accounts, offering a powerful opportunity to accelerate your savings. This week's tip is to proactively adjust your contribution strategy to take full advantage of these new higher limits. The employee contribution limit for 401(k) plans has risen to $24,500, and the limit for IRAs has increased to $7,500. For those age 50 and over, the opportunity is even greater, with catch-up provisions allowing for substantial additional savings. By planning now and increasing your deferrals, you can make a meaningful impact on your long-term financial security and ensure you are maximizing your tax-advantaged growth potential for the year.

Why This Matters

Taking advantage of increased contribution limits is crucial for several reasons. First, it directly accelerates the growth of your retirement nest egg through the power of compounding. Every extra dollar you contribute today has decades to potentially grow, and the tax-deferred or tax-free nature of retirement accounts supercharges this effect. Second, failing to adjust your contributions means leaving “free money” on the table if your employer offers a matching contribution. Many employers match a percentage of your contributions, and not contributing enough to get the full match is a common and costly mistake. This applies to anyone with access to a workplace retirement plan, but it is especially critical for those nearing retirement who need to maximize their savings in their final working years. The financial impact is substantial; consistently maxing out your contributions can translate to hundreds of thousands of additional dollars in retirement.

How to Implement

Implementing this tip requires a few straightforward steps. First, review your current contribution rate and calculate the percentage of your salary needed to reach the new $24,500 limit. For example, on a $100,000 salary, this would be 24.5% of your gross pay. If that seems too high to jump to at once, consider using your plan's auto-escalation feature to increase your contribution by 1-2% each year. Next, log in to your 401(k) provider's website or contact your HR department to adjust your contribution percentage. The timeline is immediate; make this change as early in the year as possible to spread the contributions evenly across your paychecks. If you receive a bonus, consider a front-loading strategy by contributing a large lump sum early in the year to give your money more time in the market. For those 50 and over, ensure you are also taking advantage of the catch-up contribution, which is an additional $8,000 for 401(k)s and $1,100 for IRAs in 2026. For those aged 60-63, a special “super catch-up” of $11,250 is available for 401(k)s.

Real-World Example

Consider a 52-year-old employee named Alex with a salary of $120,000. In 2025, Alex contributed $23,500 to their 401(k). For 2026, Alex decides to maximize their contributions. They increase their regular contribution to the new limit of $24,500 and also contribute the full $8,000 catch-up contribution, for a total of $32,500. This is a $9,000 increase from the previous year. Assuming a 7% average annual return, that extra $9,000 alone could grow to over $23,000 in 10 years. Now, consider a 61-year-old employee, Maria, earning $150,000. She takes advantage of the enhanced catch-up provision. She contributes the $24,500 standard limit plus the $11,250 enhanced catch-up, for a total of $35,750. This aggressive savings strategy in her final working years will have a significant impact on her retirement readiness, providing a much larger nest egg and greater financial flexibility.

Action Steps

Here is a checklist of what to do this week to implement this retirement planning tip:

- Review Your Paycheck: Log in to your payroll or 401(k) provider's portal and check your current contribution rate.

- Calculate Your New Goal: Determine the new contribution percentage required to hit the $24,500 limit for 2026.

- Adjust Your Deferral: Update your contribution settings to your new target percentage. If you are 50 or older, ensure you are also contributing to the catch-up.

- Check for Auto-Escalation: See if your plan offers an auto-escalation feature to automate future increases.

- Consult a Professional: If you are unsure about your strategy, consider speaking with a financial advisor to create a personalized plan.

Disclaimer: This content is for educational purposes only and should not be considered personalized financial or tax advice. Retirement planning is complex and highly individual. Always consult with a qualified financial advisor, tax professional, or retirement specialist before making decisions. Rules and limits change annually. The author and Market Wealth Pro do not provide personalized financial advice.