For decades, the goal was simple: save, invest, and grow. Every financial decision was filtered through the lens of accumulation, with the singular focus of building a nest egg large enough to secure a comfortable future. But what happens when that future arrives? The transition from a lifetime of saving to a lifetime of spending represents one of the most profound and often underestimated challenges of retirement. It is not merely a financial shift, but a deep psychological one, requiring a complete rewiring of the money mindset that has been ingrained for forty years or more.

This article explores the critical transition from the accumulation to the distribution phase of retirement. We will delve into the psychological hurdles that make this shift so difficult, offer practical strategies for both pre-retirees and those already in retirement, and provide a framework for creating a sustainable and enjoyable drawdown plan. Understanding and preparing for this change is the key to unlocking the peace of mind and financial confidence needed to truly thrive in your post-work years.

Understanding the Accumulation vs. Distribution Mindset

The accumulation mindset is defined by growth. Success is measured by a rising account balance, and market downturns are often viewed as buying opportunities. The core principle is to maximize contributions and let compound interest work its magic. In this phase, volatility is a friend that allows for the purchase of assets at a lower price, with a long time horizon to recover and grow.

Conversely, the distribution mindset is defined by preservation and sustainable income. The primary goal shifts from growing the nest egg to making it last for a potentially 30-plus year retirement. In this phase, market volatility becomes a significant threat. Withdrawing funds from a portfolio during a downturn can lock in losses and dramatically accelerate the depletion of assets, a concept known as “sequence of returns risk.” Success is no longer measured by the highest possible account balance, but by the consistency and reliability of the income stream it generates.

This fundamental change requires a new way of thinking. It involves moving from a singular focus on asset growth to a more nuanced strategy that balances income generation, capital preservation, and long-term growth to combat inflation. It is a transition from being a saver to becoming a strategic spender.

Common Psychological Mistakes Retirees Make

After a lifetime of disciplined saving, the act of spending can feel unnatural and even irresponsible. This leads to several common psychological mistakes that can prevent retirees from enjoying the fruits of their labor.

One of the most prevalent is the “retirement spending gap,” where retirees spend significantly less than they could sustainably afford. This is often driven by an intense fear of running out of money, a phenomenon known as loss aversion. The pain of seeing an account balance decrease, even for planned and meaningful expenses, can be more powerful than the pleasure derived from the spending itself. This can lead to a retirement of unnecessary austerity and missed opportunities.

Another common mistake is hoarding assets out of a fear of the unknown. While it is prudent to plan for unexpected expenses like healthcare costs, an excessive focus on worst-case scenarios can lead to a paralysis of spending. Many retirees struggle to give themselves “permission to spend,” even when their financial plan shows they have more than enough. This is often a direct result of the deeply ingrained habit of saving, where spending was always seen as the enemy of financial progress.

Finally, retirees can fall victim to market timing fears in a new and more dangerous way. While trying to time the market is always a risky endeavor, it can be particularly damaging in the distribution phase. Panicking and selling during a downturn, or being too conservative and missing out on necessary growth, can have irreversible consequences on the longevity of a portfolio.

Preparing for the Shift: Tips for Pre-Retirees

The years leading up to retirement are a critical time to begin preparing for the mindset shift. Taking proactive steps can make the transition smoother and less stressful.

First, create a detailed retirement budget. This is not just an academic exercise; it is a crucial step in understanding what your actual expenses will be. Track your spending for at least a year to get a realistic picture of your needs, and then project how those needs might change in retirement. This will give you a concrete number to work with and help you visualize your retirement lifestyle.

Second, begin to reframe your relationship with money. Start to think of your nest egg not as a high score to be maximized, but as a source of future income. Work with a financial advisor to create a projection of your retirement income streams, including Social Security, pensions, and portfolio withdrawals. Seeing your assets translated into a monthly “paycheck” can help you start to feel more comfortable with the idea of spending.

Third, test drive your retirement spending. In the last few years before retirement, try living on your projected retirement income. This can be a powerful reality check, helping you identify any gaps in your budget and adjust your expectations before you leave the workforce. It also provides a safe environment to practice the act of spending from your assets without the pressure of it being your only source of income.

Navigating Distribution: Strategies for Current Retirees

For those already in retirement, the key is to build confidence in your spending plan and develop strategies that allow you to spend sustainably without fear.

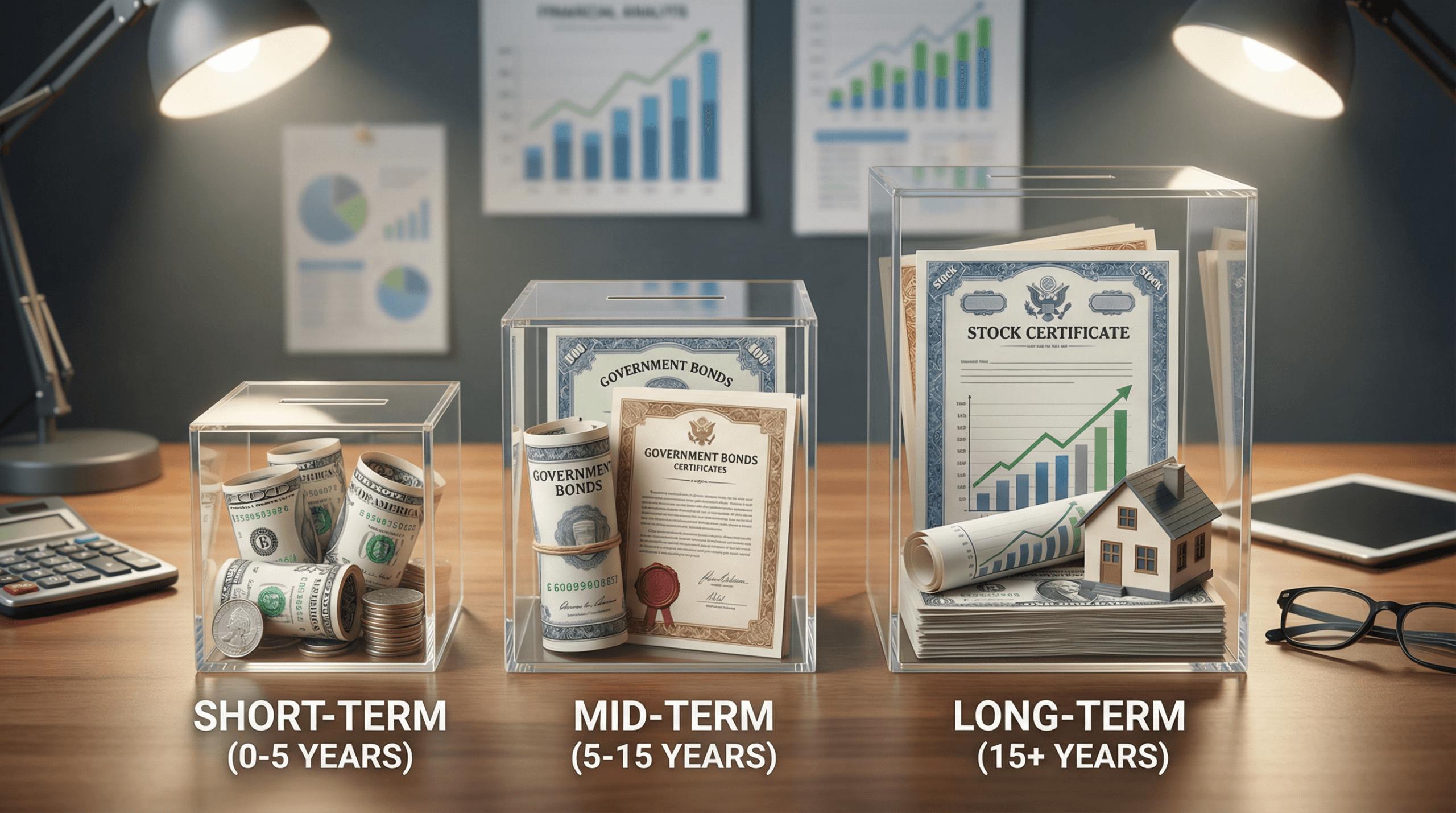

One of the most effective strategies is the “bucket approach.” This involves dividing your assets into three distinct buckets: a short-term bucket (1-3 years of living expenses in cash and cash equivalents), a mid-term bucket (3-10 years of expenses in bonds and other stable investments), and a long-term bucket (10+ years of expenses in stocks and other growth assets). This structure provides a psychological buffer, allowing you to spend from your cash bucket without worrying about short-term market fluctuations.

Another important strategy is to be flexible with your spending. The traditional 4% rule is a useful guideline, but it is not a rigid law. A dynamic withdrawal strategy, where you spend a bit less in down market years and a bit more in up market years, can significantly increase the longevity of your portfolio. This allows you to adapt to market conditions and avoid selling assets at the worst possible time.

Finally, automate your income. Set up regular, automatic transfers from your investment accounts to your checking account, just like a paycheck. This can help normalize the process of spending and reduce the emotional friction of manually selling assets. Seeing a regular, predictable income stream can provide a powerful sense of security and control.

Creating Your Sustainable Drawdown Plan

A successful drawdown plan is both a financial and an emotional document. It should be built on a solid foundation of financial analysis, but it should also reflect your personal goals and values.

Start by determining your sustainable withdrawal rate. While the 4% rule is a good starting point, it is important to customize this based on your age, asset allocation, and risk tolerance. A financial advisor can run Monte Carlo simulations to test your plan against thousands of potential market scenarios, helping you arrive at a withdrawal rate that you can feel confident in.

Next, create a tax-efficient withdrawal sequence. The order in which you tap your various accounts can have a significant impact on your after-tax returns. A common strategy is to withdraw from taxable accounts first, followed by tax-deferred accounts (like a traditional 401k or IRA), and finally tax-free accounts (like a Roth IRA). This allows your tax-advantaged accounts to continue growing for as long as possible.

Finally, review and adjust your plan regularly. Your spending needs will change over time, and market conditions will fluctuate. A retirement plan is not a static document; it is a living guide that should be reviewed at least annually with your financial advisor. This will allow you to make course corrections as needed and ensure that you stay on track to meet your long-term goals.

Final Thoughts: Finding Balance and Peace of Mind

The transition from accumulation to distribution is a journey, not a destination. It requires a conscious effort to shift your mindset from one of scarcity and saving to one of abundance and strategic spending. By understanding the psychological hurdles, preparing for the change, and implementing a sustainable drawdown plan, you can navigate this transition with confidence and grace.

Remember, you spent a lifetime building your nest egg for a reason: to provide for a comfortable and fulfilling retirement. Giving yourself permission to spend is not an act of irresponsibility; it is the final and most important step in realizing the dream you worked so hard to achieve.

Disclaimer: This content is for educational purposes only and should not be considered personalized financial or tax advice. Retirement planning is complex and highly individual. Always consult with a qualified financial advisor, tax professional, or retirement specialist before making decisions. Rules and limits change annually. The author and Market Wealth Pro do not provide personalized financial advice.