As we step into 2026, the landscape for retirement planning continues to evolve. With updated tax brackets, increased contribution limits, and a shifting interest rate environment, both pre-retirees and those already enjoying their post-work years must adapt their strategies to maximize their financial well-being. This guide provides a comprehensive overview of the key numbers and strategies you need to know to build a resilient and prosperous retirement income plan for 2026.

For Pre-Retirees: Supercharge Your Savings in 2026

For those in their final working years, 2026 offers significant opportunities to bolster your nest egg. The IRS has once again adjusted contribution limits for inflation, allowing you to save more in your tax-advantaged accounts. Maximizing these contributions is one of the most powerful levers you can pull to secure your future income.

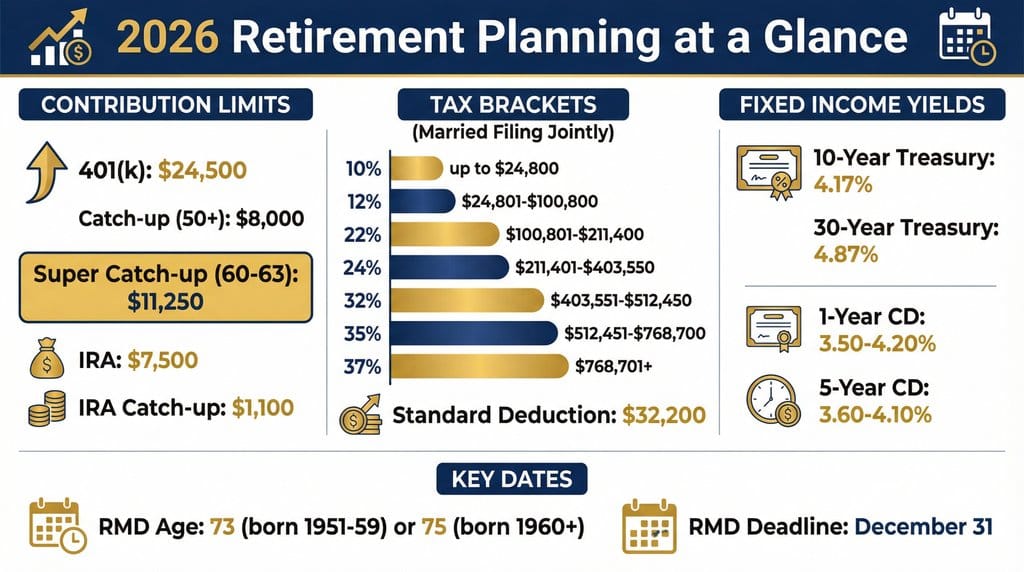

Updated 2026 Retirement Contribution Limits

Here are the key contribution limits for 2026 that every pre-retiree should aim to meet or exceed:

| Account Type | 2026 Limit | Notes |

|---|---|---|

| 401(k), 403(b), TSP | $24,500 | Up from $23,500 in 2025. |

| 401(k) Catch-Up (50+) | $8,000 | Up from $7,500 in 2025. Total contribution of $32,500. |

| 401(k) Super Catch-Up (60-63) | $11,250 | A special provision allowing even higher contributions. Total of $35,750. |

| IRA (Traditional & Roth) | $7,500 | Up from $7,000 in 2025. |

| IRA Catch-Up (50+) | $1,100 | Up from $1,000 in 2025. Total IRA contribution of $8,600. |

For Current Retirees: Navigating Withdrawals and Taxes

For those already in retirement, the focus shifts from accumulation to distribution. The primary goal is to create a sustainable income stream while minimizing your tax burden. Understanding the 2026 tax brackets and withdrawal rules is paramount.

2026 Federal Income Tax Brackets

Your retirement income, including withdrawals from traditional 401(k)s and IRAs, is taxed at ordinary income rates. Here are the 2026 brackets for single filers and those married filing jointly:

| Tax Rate | Single Filers | Married Filing Jointly |

|---|---|---|

| 10% | $0 to $12,400 | $0 to $24,800 |

| 12% | $12,401 to $50,400 | $24,801 to $100,800 |

| 22% | $50,401 to $105,700 | $100,801 to $211,400 |

| 24% | $105,701 to $201,775 | $211,401 to $403,550 |

| 32% | $201,776 to $256,225 | $403,551 to $512,450 |

| 35% | $256,226 to $640,600 | $512,451 to $768,700 |

| 37% | Over $640,600 | Over $768,700 |

The standard deduction for 2026 has also increased to $16,100 for single filers and $32,200 for married couples filing jointly, which can help shield more of your income from taxes.

Required Minimum Distributions (RMDs)

Once you reach a certain age, the IRS requires you to start taking withdrawals from your tax-deferred retirement accounts. The age for beginning RMDs is 73 for those born between 1951 and 1959, and it rises to 75 for those born in 1960 or later. Your first RMD can be delayed until April 1 of the year following the year you reach the RMD age, but all subsequent RMDs must be taken by December 31. Failing to take your RMD results in a steep 25% penalty on the amount you should have withdrawn.

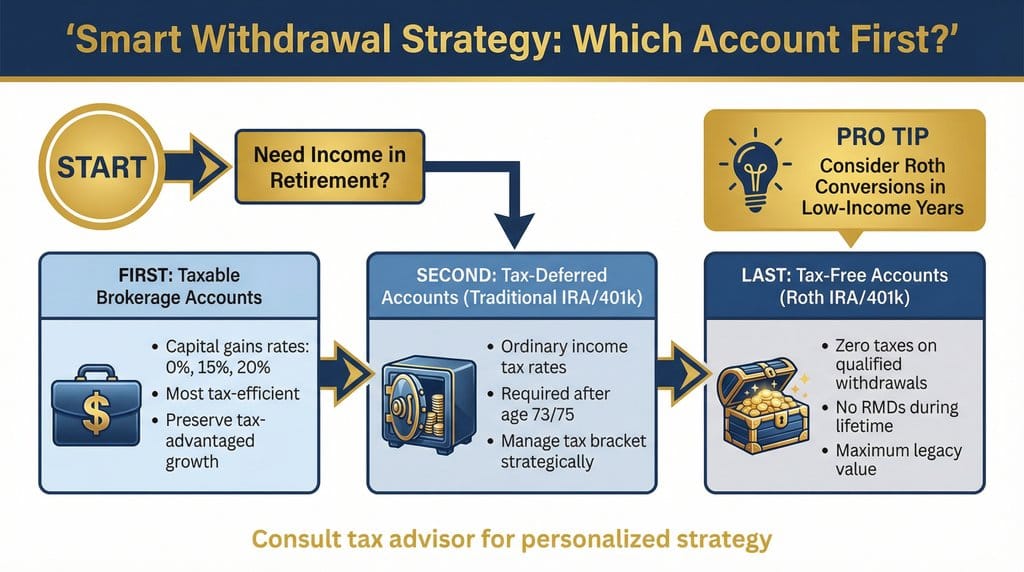

The Smart Withdrawal Strategy: Which Account to Tap First?

The order in which you withdraw from your retirement accounts can have a significant impact on how long your money lasts. Financial advisors generally recommend a specific sequence to maximize tax efficiency.

The conventional wisdom is to withdraw from your accounts in the following order:

- Taxable Brokerage Accounts: These accounts offer the most tax flexibility. You only pay capital gains taxes on the growth, and these rates (0%, 15%, or 20%) are often lower than ordinary income tax rates. Withdrawing from these accounts first allows your tax-deferred and tax-free accounts to continue growing.

- Tax-Deferred Accounts (Traditional IRA/401k): Withdrawals from these accounts are taxed as ordinary income. It's often wise to manage these withdrawals to stay within a lower tax bracket. Once you reach RMD age, you must take withdrawals from these accounts.

- Tax-Free Accounts (Roth IRA/401k): These should be your last resort. Qualified withdrawals from Roth accounts are completely tax-free, and they do not have RMDs for the original owner. This makes them a powerful tool for tax-free growth and a valuable asset to pass on to heirs.

The Role of Fixed Income in 2026

For retirees seeking stability and predictable income, fixed-income investments like bonds and CDs remain a cornerstone of a balanced portfolio. As of early 2026, yields are attractive, offering a reliable source of income to complement stock market investments.

- 10-Year Treasury Yield: ~4.17%

- 30-Year Treasury Yield: ~4.87%

- High-Yield CDs (1-5 years): 3.50% – 4.20%

These yields can provide a dependable cash flow to cover living expenses, reducing the need to sell stocks during market downturns.

Conclusion: Plan Proactively for a Prosperous 2026

Whether you are in the final stretch of your career or well into your retirement years, proactive planning is the key to financial success. By understanding the new rules for 2026, maximizing your savings opportunities, and implementing a tax-efficient withdrawal strategy, you can navigate the year with confidence and ensure your retirement income plan is built to last.

References

[1] IRS. (2025, November 13). 401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500. Retrieved from https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500

[2] IRS. (2025, October 9). IRS releases tax inflation adjustments for tax year 2026. Retrieved from https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendments-from-the-one-big-beautiful-bill

[3] Social Security Administration. (2025). Contribution and Benefit Base. Retrieved from https://www.ssa.gov/oact/cola/cbb.html

[4] Trading Economics. (2026, January 5). US 10 Year Treasury Note Yield. Retrieved from https://tradingeconomics.com/united-states/government-bond-yield