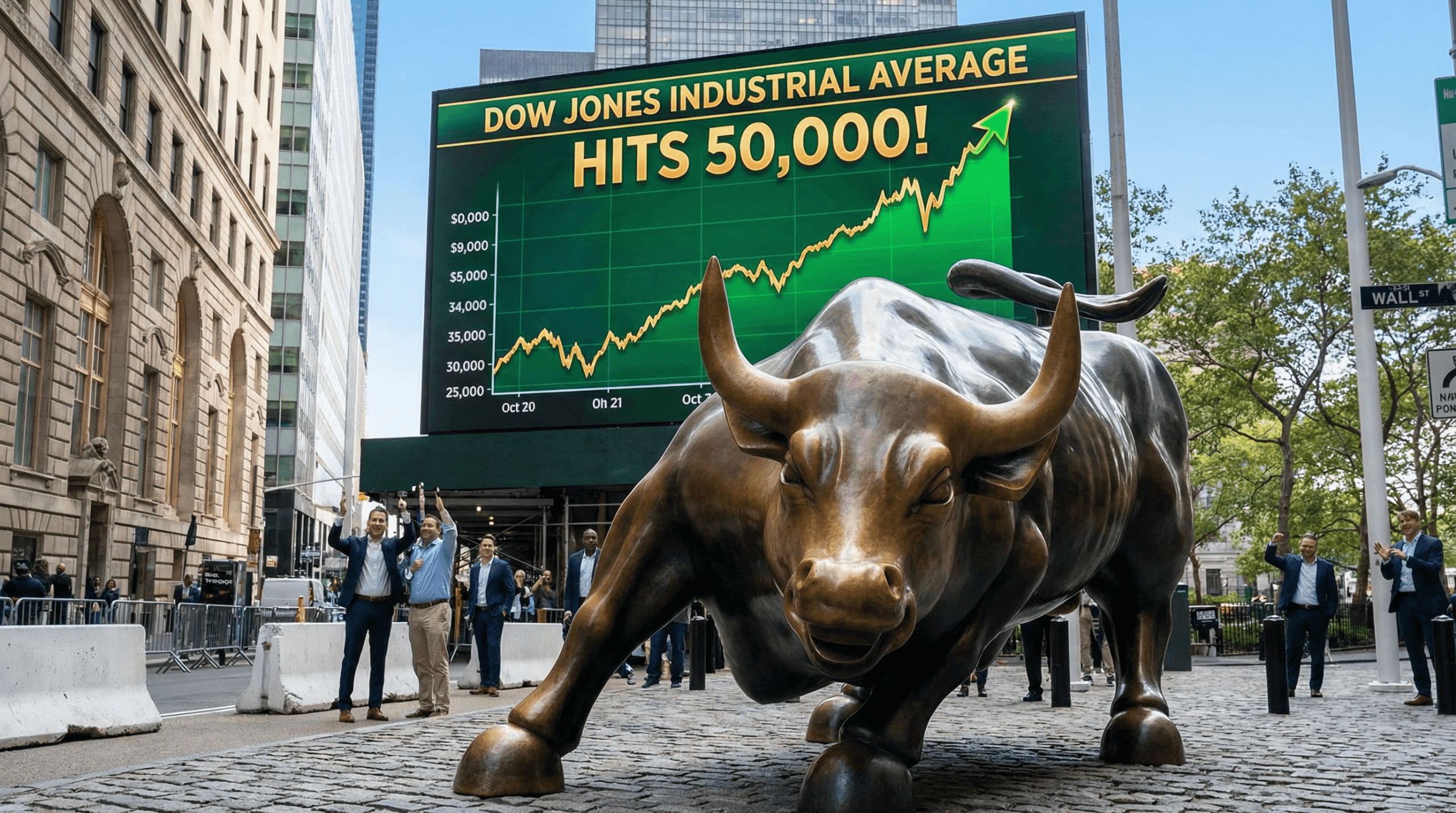

Week in Review: Dow Cracks 50,000 Amidst Tech Turmoil

The stock market experienced a week of historic milestones and significant turbulence, ultimately ending on a mixed note. The Dow Jones Industrial Average was the star performer, surging 2.5% for the week to close above the 50,000 level for the first time in history at 50,115.67. This remarkable achievement was driven by a pronounced rotation into cyclical and value-oriented stocks. In stark contrast, the technology-heavy Nasdaq Composite bore the brunt of a sector-wide sell-off, tumbling 1.8% to finish at 23,031.21. The broader S&P 500 ended the week nearly flat, with a slight decline of 0.1% to 6,932.30, reflecting the tug-of-war between the rallying value names and the plunging tech giants. The key theme of the week was the market grappling with the implications of massive AI-related spending, which fueled both excitement and fear among investors.

Top Stories of the Week

The dominant narrative this week revolved around the ballooning costs of the artificial intelligence arms race. Big Tech companies, including Amazon, Microsoft, Nvidia, Oracle, Meta, and Google, collectively saw over $1 trillion wiped from their market valuations. The sell-off was ignited by fears that the massive capital expenditures required to build out AI infrastructure could erode profitability. Amazon, in particular, sent shockwaves through the market after announcing it expects to spend a staggering $200 billion on capital expenditures in 2026, more than $50 billion above analyst expectations. This announcement alone caused Amazon's market cap to plummet by over $300 billion. The news dragged down many software stocks, with companies like ServiceNow and Salesforce hitting 52-week lows on concerns that new AI models could disrupt their traditional business models.

Investment implications: The market is clearly re-evaluating the near-term costs versus the long-term benefits of AI. While the long-term potential remains immense, investors are growing cautious about the massive upfront investments and the potential for a bubble. This environment favors companies with strong balance sheets and a clear path to monetizing their AI investments. For now, volatility in the tech sector is likely to continue as the market digests these spending plans.

Sector Performance Analysis

This week saw a dramatic rotation out of growth-oriented technology stocks and into more cyclical and value-focused sectors. Industrials and Financials were among the top-performing sectors, benefiting from the shift in investor sentiment. Shares of industrial giant Caterpillar soared 7%, while financial powerhouse Goldman Sachs gained 4%. The rally was not limited to large caps, as the Russell 2000 index of small-cap stocks also posted strong gains. The energy sector also showed strength, with ExxonMobil hitting new all-time highs. Conversely, the Technology sector was the worst performer, as evidenced by the Nasdaq's 1.8% weekly decline. The Consumer Cyclical and Communication Services sectors also faced significant headwinds, falling 3.77% and 3.7% respectively.

Investment implications: The sector rotation suggests a broadening of the market rally beyond the handful of mega-cap tech stocks that have led the market for the past year. This is a healthy sign for the overall market and suggests that investors are becoming more confident in the economic outlook. Investors may want to consider diversifying their portfolios to include more exposure to value and cyclical sectors that could benefit from a continued economic expansion.

Economic & Fed Developments

On the economic front, commentary from Federal Reserve officials provided a mixed picture. Fed Vice Chair Philip Jefferson stated that he expects U.S. GDP growth in 2026 to be around 2.2%, indicating a resilient economy. Meanwhile, San Francisco Fed President Mary Daly acknowledged “vulnerabilities” in the labor market and suggested there may be “room to cut” interest rates. In a more dovish stance, Fed Governor Stephen Miran continued to call for “aggressive” interest rate cuts. The market is currently pricing in one to two rate cuts in 2026. All eyes will be on next week's delayed January jobs report and Consumer Price Index (CPI) data, which were postponed due to a recent government shutdown. These reports will be crucial in shaping the Fed's near-term policy decisions.

Looking Ahead

The week ahead will be dominated by the release of the much-anticipated January jobs report and CPI data. These key economic indicators will provide a clearer picture of the health of the labor market and the trajectory of inflation, and will heavily influence the Federal Reserve's next move on interest rates. Investors will also be closely watching for any continuation of the sector rotation that characterized this past week. The key question is whether the rally in value and cyclical stocks has legs, or if investors will rotate back into the beaten-down technology sector. The ongoing debate around AI spending and its impact on corporate profitability will also remain a central theme, likely leading to continued volatility in the tech space.

Disclaimer: This analysis is for informational and educational purposes only and should not be considered financial advice. Past performance does not guarantee future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.