Salesforce (NYSE: CRM), the global leader in customer relationship management (CRM) software, has firmly established itself as the operating system for the modern enterprise. The company's comprehensive suite of cloud-based applications, spanning sales, service, marketing, and commerce, empowers organizations to connect with their customers in entirely new ways. At its core, Salesforce's business model is built on a recurring subscription revenue stream, providing a high degree of predictability and stability. The recent strategic acquisition of Informatica and the aggressive expansion of its Agentforce AI platform signal a pivotal evolution. The investment thesis for Salesforce centers on its ability to transition from a traditional SaaS provider to the indispensable platform for the

Agentic Enterprise, where AI agents and human employees collaborate seamlessly. By embedding intelligence directly into workflows, Salesforce is poised to capture a significant share of the burgeoning AI-driven productivity market, creating a compelling long-term growth narrative despite near-term market headwinds.

Recent Developments & Catalysts

Salesforce delivered a robust fourth quarter for fiscal year 2026, handily beating analyst expectations. The company reported revenue of $11.2 billion, a 12% year-over-year increase, and non-GAAP earnings per share of $3.81, a staggering 25% above consensus estimates. A key catalyst is the explosive growth of its AI-powered platforms. Agentforce, the company’s suite of AI tools, saw its annual recurring revenue (ARR) skyrocket by 169% year-over-year to $800 million. When combined with Data 360 and the newly acquired Informatica Cloud, the total AI-related ARR now exceeds $2.9 billion. The company closed over 29,000 Agentforce deals in the quarter alone, a 50% increase from the previous quarter, underscoring the rapid customer adoption of its AI solutions. Looking ahead, management issued confident guidance for fiscal year 2027, projecting revenues between $45.8 billion and $46.2 billion and raising its long-term FY2030 revenue target to $63 billion. Investment implications: The strong earnings beat and bullish guidance, fueled by the Agentforce hyper-growth, suggest that Salesforce is successfully monetizing its AI investments. This momentum provides a powerful catalyst that could drive a positive re-rating of the stock as the market begins to appreciate the scale of this new revenue stream.

Financial Analysis

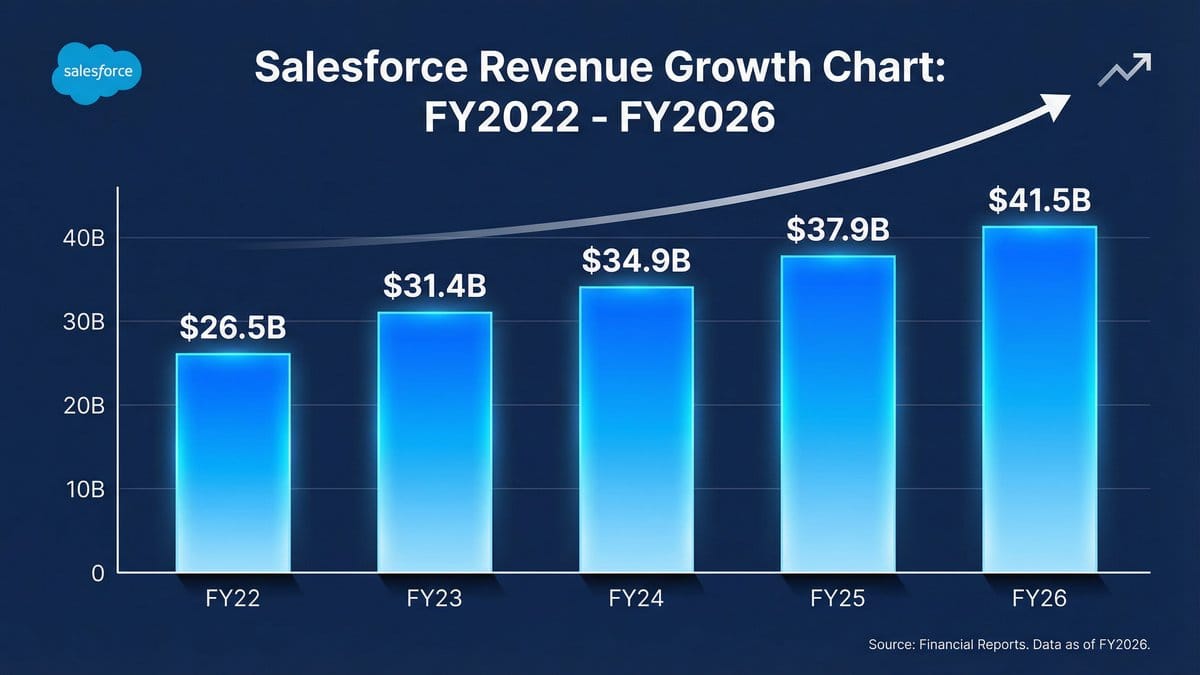

A closer look at Salesforce's financial trends reveals a company with a resilient growth profile and expanding profitability. Over the past five fiscal years, revenue has grown at a strong clip, from $26.5 billion in FY2022 to $41.5 billion in FY2026. While the growth rate has moderated from the high double digits to a projected 10-11% for FY2027, this is expected from a company of its scale and includes a roughly 3-point contribution from the Informatica acquisition. More importantly, profitability is showing significant improvement. The company achieved a non-GAAP operating margin of 34.1% in fiscal 2026 and guides for a further expansion to 34.3% in fiscal 2027. This margin expansion is a direct result of disciplined cost management and the high-margin nature of its software subscriptions. Furthermore, Salesforce is a cash-generating machine, producing $14.4 billion in free cash flow in FY2026, a 16% increase year-over-year. Investment implications: The combination of steady, profitable growth and massive free cash flow generation provides a strong foundation for shareholder returns. The company's ability to expand margins even as revenue growth matures demonstrates its operational efficiency and pricing power. This strong financial footing enables substantial capital returns, including the recently announced $50 billion share repurchase authorization.

Valuation & Competitive Position

Despite its strong fundamentals, Salesforce stock has been caught in a broader software sector sell-off, creating what appears to be a compelling valuation opportunity. As of early March 2026, the stock trades at a forward price-to-earnings (P/E) ratio of approximately 15x, a significant discount to its historical average. Its price-to-earnings growth (PEG) ratio stands near 1.0, suggesting the stock is reasonably priced relative to its expected earnings growth. The free cash flow yield is a particularly attractive 8.1%. While Salesforce faces intense competition from giants like Microsoft and ServiceNow, its entrenched position as the #1 CRM provider affords it a durable competitive moat. The platform's stickiness, high switching costs, and vast ecosystem of developers and partners create a powerful network effect. The company is not standing still; it is actively evolving to counter threats by positioning Agentforce as the central nervous system for enterprise AI, a strategy aimed at moving up the value chain from simple seat-based licenses to high-value, usage-based AI workflows. Investment implications: The current valuation does not appear to fully reflect the company's dominant market position or the massive growth potential of its Agentforce platform. For long-term investors, the disconnect between the stock's price and the company's intrinsic value presents an attractive entry point. The market's focus on near-term SaaS headwinds may be obscuring the long-term value creation from its AI-driven transformation.

Risks & Outlook

The primary risk to the investment thesis is the potential for AI to disrupt Salesforce's traditional seat-based business model more rapidly than anticipated. If AI-native competitors or autonomous agents can replicate core CRM functions at a lower cost, it could pressure pricing and lead to customer churn. Additionally, the company's revenue growth has decelerated, and its guidance for fiscal 2027, while strong, was slightly below some of the more bullish analyst expectations. Integrating the large Informatica acquisition also presents execution risk. However, the outlook remains positive. Salesforce is proactively addressing the AI threat by becoming a leader in the agentic AI space itself. The company expects an organic revenue re-acceleration in the second half of fiscal 2027. Its massive $50 billion buyback program should provide strong support for the stock, and its push into high-value government contracts with its Missionforce unit opens up a new, lucrative market. While the transition involves risks, Salesforce's strategic pivot, dominant market position, and attractive valuation present a favorable risk/reward profile for investors.

Disclaimer: This analysis is for informational and educational purposes only and should not be considered financial advice. Individual stock investments carry significant risks including company-specific and market risks. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.