> Disclaimer: This article is for informational and educational purposes only. It does not constitute tax, legal, or financial advice. The world of digital asset taxation is complex and subject to change. Please consult with a qualified tax professional or CPA specializing in cryptocurrency to address your specific situation.

As a crypto investor, earning passive income through staking is one of the most attractive features of the digital asset ecosystem. However, with great rewards comes great tax responsibility. The IRS has significantly increased its focus on crypto compliance, and for the 2026 tax season (reporting on 2025 activity), new rules are coming into effect that every staker must understand. Ignoring these obligations can lead to steep penalties and unwanted attention from tax authorities. This guide will walk you through the essential tax implications of crypto staking for 2026, helping you stay compliant and navigate the rules with confidence.

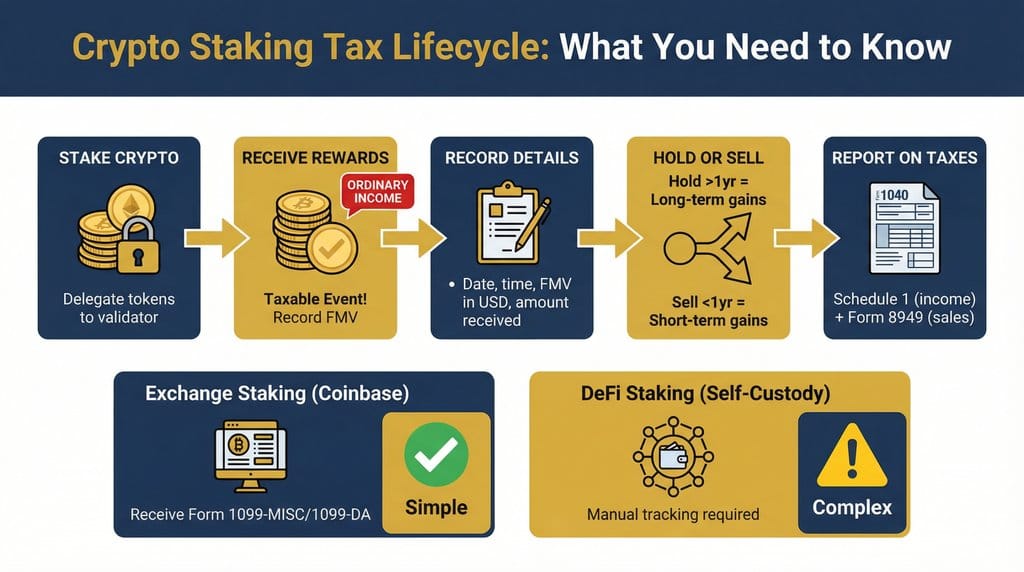

The Two-Step Rule: How Staking Rewards Are Taxed

The fundamental principle of staking taxation in the U.S. is a two-step process. It's crucial to understand both steps, as they represent two separate taxable events.

Step 1: Ordinary Income at Receipt

The moment you gain “dominion and control” over your staking rewards, they are considered ordinary income. “Dominion and control” simply means you are free to sell, trade, or move the tokens. The amount of income you must report is the fair market value (FMV) of the rewards in U.S. dollars at the exact time you received them. This income is reported on Schedule 1 of your Form 1040, and there is no minimum threshold; every dollar must be reported. [1]

Step 2: Capital Gains or Losses at Disposal

The FMV you recorded at receipt becomes your cost basis for those specific tokens. When you later sell, swap, or spend those tokens, you trigger a second taxable event. You will realize a capital gain or loss, calculated as the difference between your cost basis and the value you received upon disposal. If you hold the tokens for more than a year, it's a long-term capital gain (taxed at lower rates). If you hold for a year or less, it's a short-term capital gain (taxed at your ordinary income rate). [2]

The New Rules for 2026: Understanding Form 1099-DA

The biggest change for the 2026 tax season is the introduction of Form 1099-DA, Digital Asset Proceeds from Broker Transactions. For transactions occurring in 2025, centralized exchanges (brokers) like Coinbase, Kraken, and Gemini will be required to report the gross proceeds from digital asset sales to both you and the IRS. Starting with 2026 transactions, they will also be required to report your cost basis. [3]

However, the IRS has issued temporary relief (Notice 2024-57) stating that brokers are not required to report staking transactions themselves on Form 1099-DA until further guidance is issued. This is a critical distinction: while the act of staking isn't reported by the broker, the staking rewards you receive are still considered income and may be reported on a Form 1099-MISC if you earn over $600 from a single platform. Regardless of whether you receive a form, you are still legally obligated to report all staking income. [4]

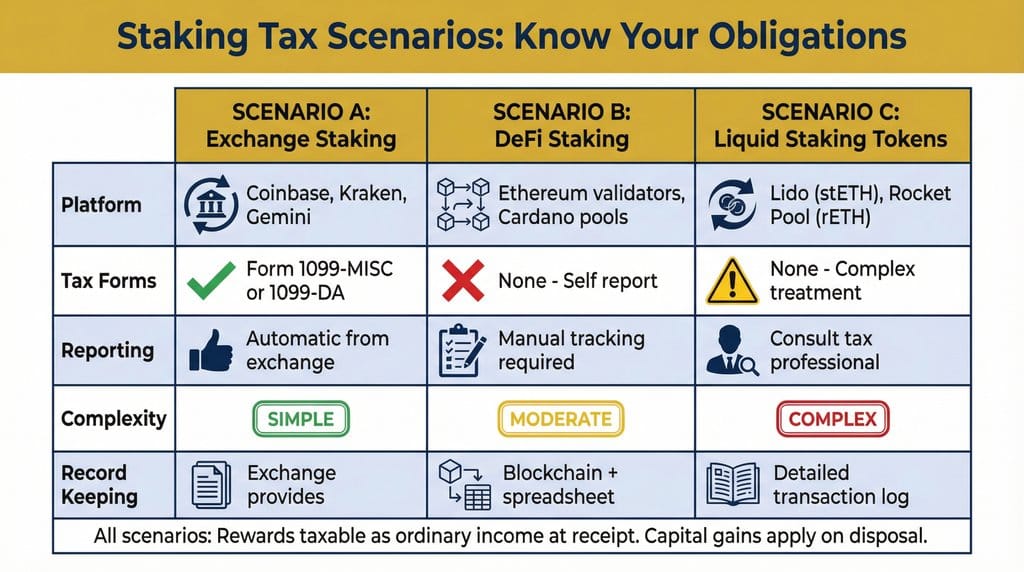

Staking on Exchanges vs. DeFi: A Tale of Two Scenarios

Your reporting obligations vary significantly depending on where you stake your assets. Staking on a centralized exchange is far simpler from a tax perspective than staking in a self-custody wallet within the world of Decentralized Finance (DeFi).

Scenario A: Centralized Exchange Staking

This is the most straightforward scenario. The exchange tracks your rewards and will likely provide you with tax forms (like Form 1099-MISC) and end-of-year summary reports. While convenient, you must still reconcile these forms with your own records to ensure accuracy.

Scenario B: DeFi Staking

When you stake in a self-custody wallet, you are your own broker. No one will be sending you tax forms. You are solely responsible for tracking every single reward transaction. This requires meticulous record-keeping, including the date, time, amount, and FMV of every reward received. Tools like blockchain explorers and crypto tax software become essential for compliance.

Navigating Complex Scenarios

The world of staking is filled with complex products that create tax uncertainty. Here are two common examples:

- Liquid Staking Tokens (LSTs): When you stake ETH on a platform like Lido, you receive stETH in return. The IRS has not issued clear guidance on whether this initial transaction is a taxable event. A conservative approach would treat it as a taxable swap, while a more aggressive stance might argue no tax is due until the stETH is sold or redeemed. Given the ambiguity, consulting a tax professional is highly recommended.

- Auto-Compounding Rewards: Some protocols automatically re-stake your rewards. Even though you don't manually claim them, you likely have “dominion and control” the moment they are added to your staked balance. Each compounding event is a new taxable income event that must be tracked.

Record-Keeping and Tax Planning Strategies

Given the IRS's increased scrutiny, meticulous record-keeping is your best defense. For every staking reward, you should record:

- The date and time of receipt.

- The type and amount of cryptocurrency received.

- The fair market value (in USD) at the time of receipt.

- The transaction ID from the blockchain.

To manage your tax liability, consider strategies like tax-loss harvesting, where you sell assets at a loss to offset capital gains. Additionally, making quarterly estimated tax payments can help you avoid underpayment penalties if you have significant staking income.

The Cost of Non-Compliance

The IRS is no longer taking a lenient stance on crypto tax evasion. The question “At any time during [the tax year], did you receive, sell, send, exchange, or otherwise acquire any financial interest in any digital asset?” is prominently featured on Form 1040. Failure to report accurately can result in accuracy-related penalties (20% of the underpayment), fraud penalties (75% of the underpayment), and in severe cases, criminal prosecution. [5]

Conclusion: Proactive Compliance is Key

The tax implications of crypto staking are complex but manageable. The key to staying compliant in 2026 and beyond is to understand the two-step tax rule, meticulously track every transaction, and be aware of the new broker reporting requirements. Whether you are a casual staker on an exchange or a DeFi power user, proactive record-keeping and a clear understanding of your obligations will save you from significant stress and potential financial penalties down the road.

> Final Reminder: The information in this guide is intended for educational purposes. Always consult with a qualified tax professional who specializes in digital assets to ensure you are meeting your specific tax obligations.

References

[1] Gordon Law Group. (2025). Crypto Staking Taxes 101. Retrieved from https://gordonlaw.com/learn/crypto-staking-taxes/

[2] TokenTax. (2025, October 29). Crypto Staking Taxes 2026: The Complete Guide. Retrieved from https://tokentax.co/blog/crypto-staking-taxes

[3] Internal Revenue Service. (2024, June). Final regulations and related IRS guidance for reporting by brokers on sales and exchanges of digital assets. Retrieved from https://www.irs.gov/newsroom/final-regulations-and-related-irs-guidance-for-reporting-by-brokers-on-sales-and-exchanges-of-digital-assets

[4] Internal Revenue Service. (2024). Notice 2024-57. Retrieved from https://www.irs.gov/pub/irs-drop/n-24-57.pdf

[5] Internal Revenue Service. (2023). Digital assets. Retrieved from https://www.irs.gov/filing/digital-assets