1. S&P 500 Hits Record Highs as Markets Close 2025 on Strong Note

The S&P 500 achieved two new record highs last week, extending its bull run to a potential seven-month streak with an impressive 87.5% gain since October 2022. The index rose 1.4% for the week, while the Dow Jones Industrial Average climbed 1.2%, both reaching fresh all-time highs. The rally was led by the familiar “Magnificent Seven” technology stocks, with mega-cap growth names like Nvidia driving momentum despite some notable declines in Tesla and Bitcoin. Wall Street's most optimistic strategists now forecast the S&P 500 could reach 8,100 in 2026, representing potential upside of 18% from current levels.

Why it matters for investors: This record-breaking performance underscores the market's resilience heading into 2026, but it also highlights growing concentration risks. The narrow leadership from a handful of mega-cap technology stocks means portfolio diversification has become increasingly challenging. Investors must weigh the momentum of AI-driven growth stocks against elevated valuations, with the Nasdaq 100 now trading at over 30 times earnings. The continued outperformance of large-cap growth over small-caps and equal-weighted indices suggests that maintaining exposure to market leaders remains critical for portfolio performance, even as valuation concerns mount.

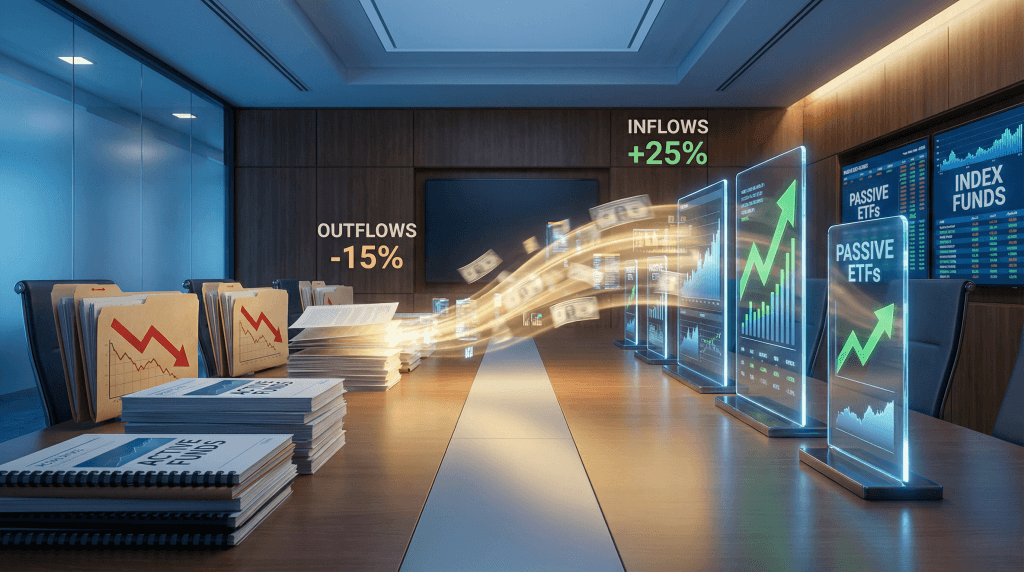

2. Trillion-Dollar Exodus from Active Mutual Funds Accelerates

Around $1 trillion was pulled from active equity mutual funds in 2025, marking the 11th consecutive year of net outflows and potentially the steepest exodus of the cycle, according to Bloomberg Intelligence estimates. Meanwhile, passive equity exchange-traded funds attracted more than $600 billion in inflows. The data reveals that 73% of equity mutual funds trailed their benchmarks this year, the fourth-worst performance since 2007. The concentration of returns in just a handful of mega-cap technology stocks made it exceptionally difficult for diversified active managers to keep pace with index funds.

Why it matters for investors: This massive capital rotation from active to passive strategies has profound implications for market structure and individual portfolio construction. The trend suggests that paying higher fees for active management has become increasingly difficult to justify when a small group of stocks dominates index returns. Investors should critically evaluate their fund holdings and fee structures, considering whether active managers can truly add value in a market where concentration has reached extreme levels. The shift also raises concerns about market efficiency and price discovery, as passive flows indiscriminately buy the largest stocks regardless of valuation, potentially amplifying momentum and creating future volatility when sentiment shifts.

3. China Signals Sustained Fiscal Support Amid Economic Headwinds

China's Finance Ministry announced plans for more “proactive” fiscal policies in 2026, with authorities pledging to refine their mix of government bond tools to improve effectiveness and continue supporting the national consumer goods trade-in program. This announcement comes as China's industrial profits tumbled at their fastest pace in over a year, with the economy estimated to have grown by just 2.5-3% in 2025 according to the Rhodium Group think tank, roughly half the pace implied by official data. Cash-strapped local governments drove record sales of asset-backed securities, with 2,386 deals completed as of December 24, surpassing the previous record set in 2021.

Why it matters for investors: China's economic struggles and policy response have far-reaching implications for global markets, commodity prices, and multinational corporate earnings. The combination of weak industrial profits, slowing growth, and aggressive local government financing through asset-backed securities signals deep structural challenges in the world's second-largest economy. Investors with exposure to emerging markets, commodities, or companies with significant China revenue should closely monitor these developments. The fiscal stimulus measures may provide short-term support, but the effectiveness remains uncertain given persistent property sector weakness and potential tariff headwinds. This situation could create opportunities in select Chinese equities if stimulus proves effective, but also poses significant downside risks if economic conditions deteriorate further.

4. US Dollar Posts Worst Week Since June as Rate Cut Expectations Rise

The US dollar capped its worst week since June, with the Bloomberg Dollar Spot Index falling 0.8% for the week and declining approximately 8% for the full year, marking what would be its steepest annual drop. The currency weakness coincided with a decline in Treasury yields, with US 10-year yields falling about two basis points to 4.13%. Traders are pricing in approximately 90% probability that the Federal Reserve will hold rates steady in January, but they're betting on another quarter-point cut by mid-year and one more later in 2026, with the federal funds rate expected to settle around 3.0-3.5%.

Why it matters for investors: Dollar weakness has significant portfolio implications across multiple asset classes. A declining dollar typically benefits international stocks, emerging market equities, commodities priced in dollars (like gold and oil), and US multinational corporations with substantial foreign revenue. Investors should consider increasing international diversification to capitalize on currency tailwinds and the potential for non-US markets to outperform. However, dollar weakness also reflects concerns about US fiscal sustainability, with national debt surpassing $38 trillion, and potential de-dollarization trends as central banks diversify reserves. Fixed-income investors should be particularly attentive to how currency movements affect real returns, while equity investors may find opportunities in export-oriented US companies and international markets that benefit from a weaker greenback.

5. Germany's Unemployment Crisis Deepens as Economic Malaise Spreads

Germany's job placement indicator fell to its lowest level on record, with unemployment surpassing 3 million in August and more than 100,000 additional people entering the job market in November compared to the same period last year. The Halle Institute for Economic Research estimates that around 170,000 positions have been affected in 2025, up from fewer than 100,000 before the COVID-19 pandemic. German industry has shed almost 250,000 jobs in a worsening downturn driven by weak foreign demand, high interest rates, and a prolonged energy crisis, with the economy stuck in recession since late 2022.

Why it matters for investors: Germany's economic crisis poses serious risks to European growth prospects and the eurozone's stability, given Germany's role as the region's largest economy and traditional growth engine. The combination of rising unemployment, industrial decline, and recession creates headwinds for European equities, particularly in manufacturing, industrials, and export-oriented sectors. However, this weakness may accelerate pressure on the European Central Bank to cut interest rates more aggressively, potentially supporting bond prices and rate-sensitive sectors. Investors should be cautious about exposure to European cyclical stocks and consider that Germany's malaise could spread to neighboring economies. The situation also highlights the importance of Europe's need for structural reforms and the potential for fiscal stimulus, which could create opportunities if Germany's new government implements aggressive spending measures to revive growth.