The U.S. economy presents a complex and somewhat contradictory picture as of late January 2026. While headline GDP growth figures suggest a period of robust expansion, a closer look at underlying indicators reveals a more nuanced reality. Inflationary pressures, while moderating, remain stubbornly above the Federal Reserve's target, and the labor market is showing signs of cooling after a period of rapid growth. This analysis will delve into the key data points shaping the current economic landscape, exploring the intricate balance between growth, inflation, and employment, and what it means for investors and the market outlook.

Inflation & Fed Policy: A Delicate Balancing Act

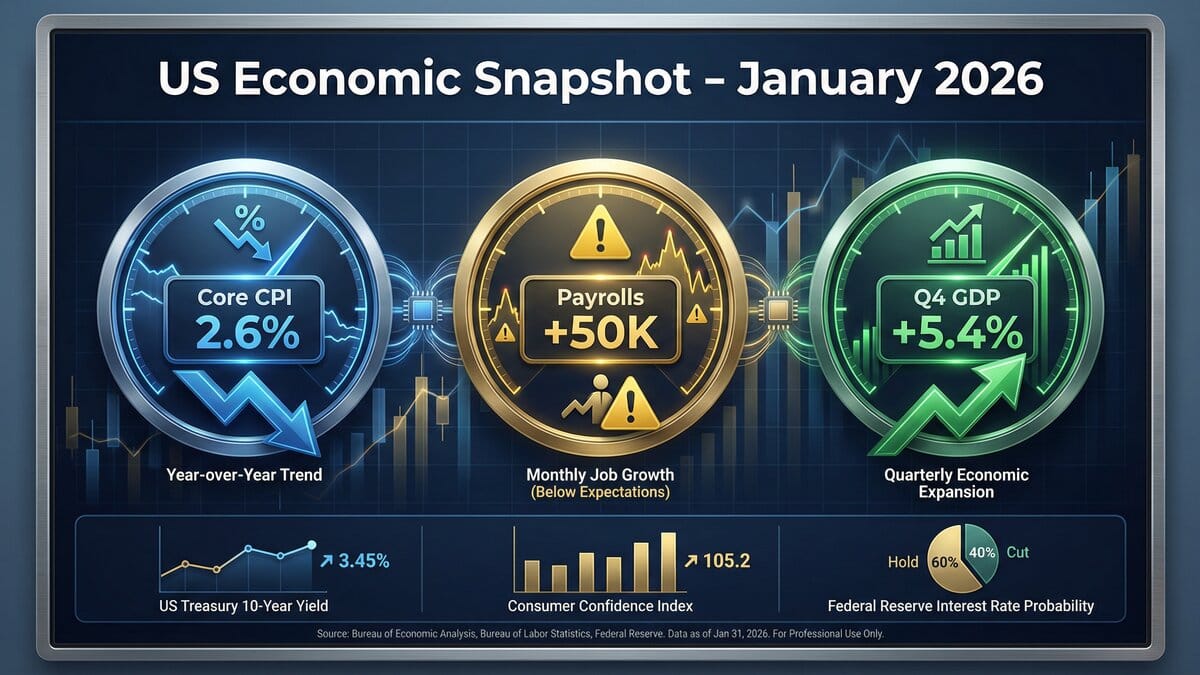

Inflation continues to be a primary focus for policymakers and investors alike. The latest Consumer Price Index (CPI) data for December 2025 showed a continued, albeit slow, moderation in price pressures. The core CPI, which excludes volatile food and energy prices, rose 0.2% for the month and 2.6% on an annual basis. While these figures were slightly below expectations, they remain above the Federal Reserve's 2% target. Headline CPI, which includes all items, rose 0.3% monthly and 2.7% annually, aligning with consensus estimates. A significant contributor to persistent inflation is the shelter category, which saw a 0.4% monthly increase and a 3.2% rise year-over-year. This component, which makes up a substantial portion of the CPI, has proven to be particularly sticky. In contrast, some goods are experiencing deflationary pressures, with used car prices falling 1.1% and new vehicle prices remaining flat. The Fed's preferred inflation gauge, the Personal Consumption Expenditures (PCE) price index, is expected to show core inflation holding at 2.8%, reinforcing the central bank's cautious stance. After a series of three rate cuts in late 2025, the Federal Reserve has signaled a pause, holding the federal funds rate in the 3.50% to 3.75% range. The market consensus is that the Fed will remain on hold through the first half of 2026, with a potential rate cut not materializing until at least June. This patient approach reflects the delicate balance the Fed must strike between curbing inflation and avoiding a significant economic downturn.

Investment implications: The current inflationary environment and the Fed's policy response have significant implications for investment strategies. With the central bank on an extended pause, the yield curve is likely to remain a key focus. A prolonged period of elevated, albeit moderating, inflation could favor investments in real assets and inflation-protected securities. Sectors with pricing power may also outperform. However, the risk of a policy mistake, where the Fed either tightens too much or too little, remains a significant concern for equity and bond markets.

Labor Market: Signs of Cooling

The U.S. labor market, a pillar of strength throughout the post-pandemic recovery, is now exhibiting clear signs of cooling. The December 2025 jobs report indicated that nonfarm payrolls increased by a modest 50,000, falling short of expectations. This brought the total job gains for 2025 to 584,000, the weakest annual performance since 2020. The unemployment rate, however, edged down to 4.4%, with the total number of unemployed persons at 7.5 million. While the headline unemployment number remains low by historical standards, the slowdown in job creation suggests a loss of momentum. Sector-specific data reveals a diverging landscape. Job growth continued in food services and drinking places, health care, and social assistance. In contrast, the retail trade sector shed 25,000 jobs, reflecting a potential shift in consumer spending patterns. Average hourly earnings continued to rise, with a 0.3% monthly increase, but the pace of wage growth has moderated from its recent peaks. The overall picture is one of a labor market that is rebalancing, moving from a state of overheating to one of more sustainable, albeit slower, growth.

Investment implications: A cooling labor market has mixed implications for investors. On one hand, it eases concerns about wage-driven inflation, which could give the Federal Reserve more flexibility. On the other hand, a significant slowdown in job growth could signal a broader economic downturn, which would be negative for corporate earnings and stock prices. Investors should closely monitor labor market indicators for signs of either stabilization or further deterioration. A gradual cooling could be a positive for markets, supporting the “soft landing” narrative. However, a sharp increase in unemployment would be a major red flag.

Growth & Consumer: Resilient but Cautious

Despite the cooling labor market, U.S. economic growth has remained surprisingly resilient. The final reading for Q3 2025 GDP showed a strong annualized growth rate of 4.3%. More strikingly, the Atlanta Fed's GDPNow model is forecasting a remarkable 5.4% growth rate for Q4 2025. This robust growth is supported by strong productivity gains, which surged by 4.9% in the third quarter, the strongest reading in nearly six years. This has allowed the economy to grow without a significant increase in inflationary pressures, a scenario often referred to as a “Goldilocks economy.” Consumer spending has also held up well, with retail sales in November exceeding expectations. However, there are signs of caution. The Federal Reserve's Beige Book noted that while consumer spending on retail and travel increased moderately, auto sales declined. There is also anecdotal evidence of a “no-buy January” trend, suggesting that consumers may be pulling back on spending after the holiday season. The outlook for 2026 is for continued, albeit more moderate, growth. The IMF projects global growth of 3.3% for the year, with the U.S. expected to outperform many of its peers.

Investment implications: The strong GDP growth and productivity gains are positive for corporate earnings and could support equity markets. However, the sustainability of this growth is a key question. If consumer spending begins to falter, it could weigh on economic growth and corporate profits. Investors should focus on companies with strong balance sheets and resilient business models that can weather a potential slowdown in consumer demand. The divergence between strong GDP growth and a cooling labor market also warrants attention. This could be a sign of a productivity-driven expansion, which would be a long-term positive for the economy and markets.

Market Implications & Outlook

The current economic data presents a complex and, at times, contradictory narrative for financial markets. The moderation in inflation and the cooling of the labor market have been welcomed by investors, as they reduce the pressure on the Federal Reserve to pursue a more aggressive tightening policy. This has led to a decline in Treasury yields and a rally in stock prices. The surprisingly strong GDP growth and productivity gains have also provided a tailwind for risk assets. However, significant uncertainties remain. The persistence of shelter inflation, the potential for a sharper-than-expected slowdown in the labor market, and the risk of a consumer retrenchment all pose threats to the current market optimism. The political landscape, with potential pressure on the Federal Reserve, adds another layer of complexity. Looking ahead, the market is likely to remain highly data-dependent, with each new economic release being closely scrutinized for clues about the future direction of the economy and Fed policy. The base case scenario appears to be a “soft landing,” where inflation returns to target without a major recession. However, the risks of a less benign outcome are not insignificant. Investors should maintain a balanced and diversified portfolio, with a focus on quality and resilience.

Disclaimer: This analysis is for informational and educational purposes only and should not be considered financial advice. Economic forecasts are subject to significant uncertainty and actual results may differ materially. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.